CFP Who Was A Consulting Actuary Taught Himself Programming And His New Software Is Simple, Effective, And Adds A New Twist To Finding A Safe Retirement Withdrawal Rate Hot

Write Review

The Retirement Planner By RetireSoft

Zolt turned retirement income planning on its head to come up with a new way to solve the math problem of finding a retiree’s safe withdrawal rate. “It’s a paradigm shift,” says Zolt, 58.

Zolt says traditional financial planning software apps approach retirement income planning by starting with a retirement age assumption and then telling you whether you’re spending too much or too little. The retirement age is a fixed target in traditional retirement planning software.

Zolt’s software solves the math problem that is retirement income in a different way. By solving for the safe retirement withdrawal rate instead of starting with a specific target rate of withdrawal, Zolt has done something seemingly simple that adds an important twist in the retirement planning process.

“Retirement planning is an equation with about seven variables: portfolio size, portfolio return, savings, living expenses including taxes, years to retirement, and withdrawal rate,” says Zolt. “To solve the problem, you need to fix or assume certain variables in order to solve for other variables.”

“This is where the science becomes art, and where my approach is new and novel,” Zolt adds. “I have chosen to make the number of years to retirement the variable and solve for the withdrawal rate. The result is a simple demonstration that clients can easily follow and, in turn, buy into, which is a key component in client relationships.”

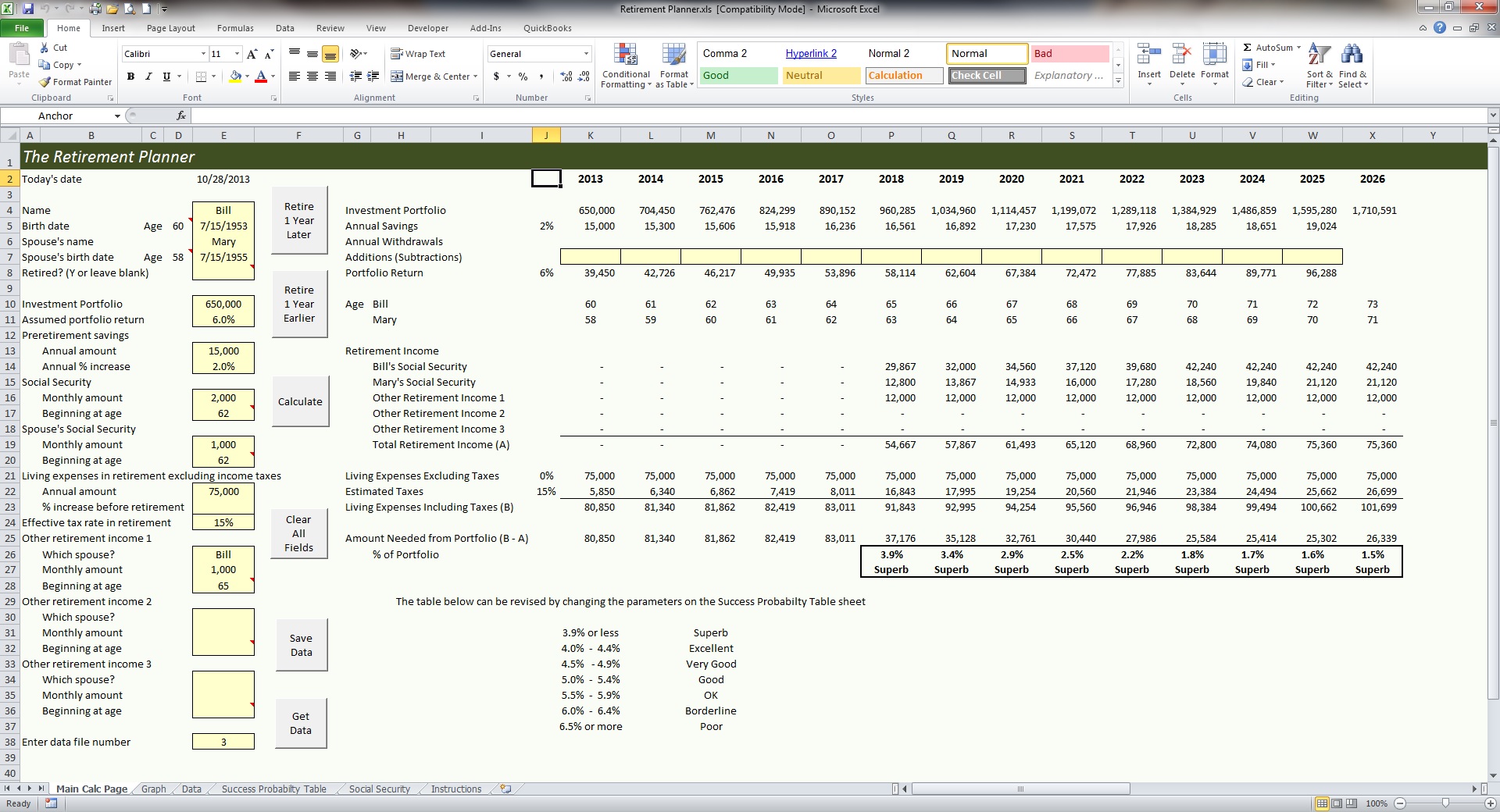

Above is a screenshot of the most complicated spreadsheet in The Retirement Planner. By changing the one of the variables of the retirement income planning equation, advisors can instantly tweak “what if” scenarios. It’s dead simple. Zolt has done all the math and programmed the spreadsheet himself. He’s locked it down so you can’t see the code without hacking it hard.

Take a look at the 7½-minute video demo that Zolt gave me of the app and tell me what you think. It looks like this is a really simple, low cost way for advisors to work on a retirement case on the fly with a client.

Zolt will be speaking in detail about his new approach on Friday, Feb. 7 at 4 p.m. at a webinar that is free to A4A members ($60) and that will be eligible for professional education credit

Zolt Is Emblematic Of A Big Change In Financial Advisor Technology

Zolt is just the guy you want to calculate safe withdrawal rates for retirees. He’s an Associate of the Society of Actuaries and a member of the American Academy of Actuaries and he’s also an Enrolled Agent. For 25 years he worked as a consultant at Coopers & Lybrand, Foster Higgins, and Buck Consultants, and he became a team leader managing small groups of retirement plan consultants who billed out at $600 an hour.

In 2004, he was downsized and retired as a consulting actuary to start a financial planning practice in Westlake, Ohio. He can retire but he thinks retirement math is fun and loves keeping busy with financial planning.

Zolt says he works on a retainer basis for 18 clients and does projects as needed for another 12. Zolt says has not taken a new client for a year. That’s because he’s been busy working on the software.

In January 2013, Zolt authored an article published in The Journal of Financial Planning about how the 4% safe withdrawal rate relied on as a rule of thumb by many practitioners could actually be stretched to 6% with some minor tweaks without increasing the risk of running out of money. He then did some public speaking explaining the article, and practitioners asked him how they could implement his ideas. That got him thinking and led to him to his upside-down approach to solving the safe-withdrawal rate problem.

With just 12 official office-hours a week, Zolt spent the summer of 2013 learning Visual Basic for Applications (VB), which allows you to write code for Excel spreadsheets, by taking tutorials and doing research online. While Zolt had previously written Excel macros with 10 or 15 lines of code, the VB code powering his spreadsheet contains about 1000 lines of code, he says. He hired a consultant show him how to lock down the code so nobody can see it unless they pay him $99 for the year and $79 annually thereafter.

By the end of last summer, Zolt had introduced The Retirement Planner app to members of the Alliance of Cambridge Advisors (ACA), a group of fee-only financial planners who share a practice methodology and other ideas, a group that Zolt raves about. Some ACA advisors became beta testers and 25 are now using the spreadsheet, which is up to version 1.2.

“I had a second Retirement Planning meeting with a client recently,” according to a testimonial on RetireSoft’s website from an ACA advisor. “At the first meeting, we went over their retirement picture using (the ACA Retirement Analyzer) and MoneyGuidePro. This time I used your Retirement Planner, and they loved it!!! They gushed about how user friendly it was, and how clear the results were. Thank you very much!!”

Zolt says he is “having a blast.” That’s because he’s a math-murderer. He kills this stuff. When he was four-years old, he says, his parents would play a game with him where they would give him a date in history and he would tell them what day of the week it fell on. “For me I am a financial planner and come home from my job and play with spreadsheets,” says Zolt. “This is what I do to unwind.”

Software for financial advice professionals can now be coded by people who are not professional programmers but who learn a bit of programming to do it themselves, or who learn enough about how to code to not get snookered by programmers they hire. It is spawning new professional apps that are simple and inexpensive and built to do one thing well.

What Manish Malhotra is doing with Income Discovery, David Zolt is doing with RetireSoft, and other individuals with a big idea are doing elsewhere could be disruptive to large software vendors and alter the technology choices for financial planning practitioners. It has become so easy for a one-man operation to build software for a small targeted group of financial advisors and sell it at a fraction of the price of apps from traditional professional software companies with 10, 20 or 30 employees or more. That’s going to continue to make financial planning and investment advising a very fragmented field and allow for advisors to differentiate themselves based on the way they practice.

This Website Is For Financial Professionals Only

User reviews

There are no user reviews for this listing.