Powerful Graphics to Wow Clients at This Year’s Investment Performance Reviews Hot

Here's a summary of what the graphs show:

Stock Markets in 2010

U.S.

- The total market (5000 stocks) returned 18%. The S&P500 lagged with a 15% return.

- Smaller companies were in favor, returning more than 20%, while large companies returned "only"13%.

- Materials and Consumer Discretionary companies performed best, earning 35% and 30% respectively. Health Care and Consumer Staples lagged with 6% and 9% returns.

Foreign

- The total market (20,000 stocks) earned 17.5%, more than doubling the EAFE (900 stocks) index's 8.2% return.

- Small-to-mid (Smid) value was in favor, earning 30%, while large companies returned 12%.

- Latin America and Emerging Markets led with 40% and 28% returns, respectively, while Europe-ex-UK lagged with a 5% return.

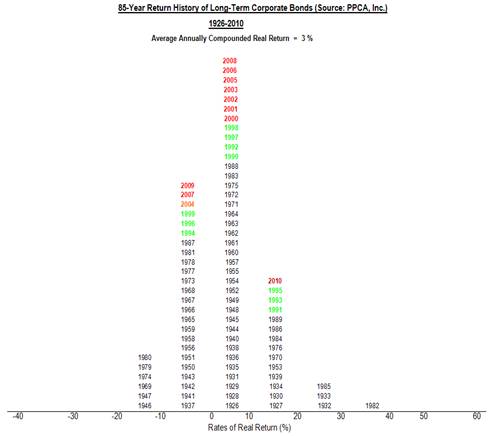

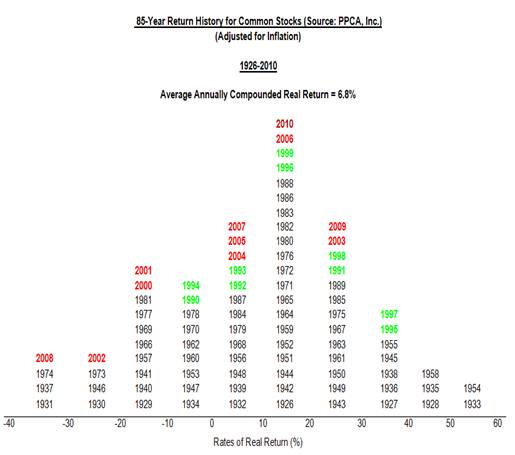

The 85-year History of the US Stock and Bond Markets

- US stock market performance in 2010 was right in the middle of its historical range. It was a typical year.

- US bond performance was quite good, better than average.

The Year 2010 in Review

I review the year by analyzing why popular indexes, namely the S&P500 and the EAFE, performed as they did. I provide attribution analyses set against a backdrop of the entire market. Advisors can integrate these insights into their annual performance reviews.

US Stock Market

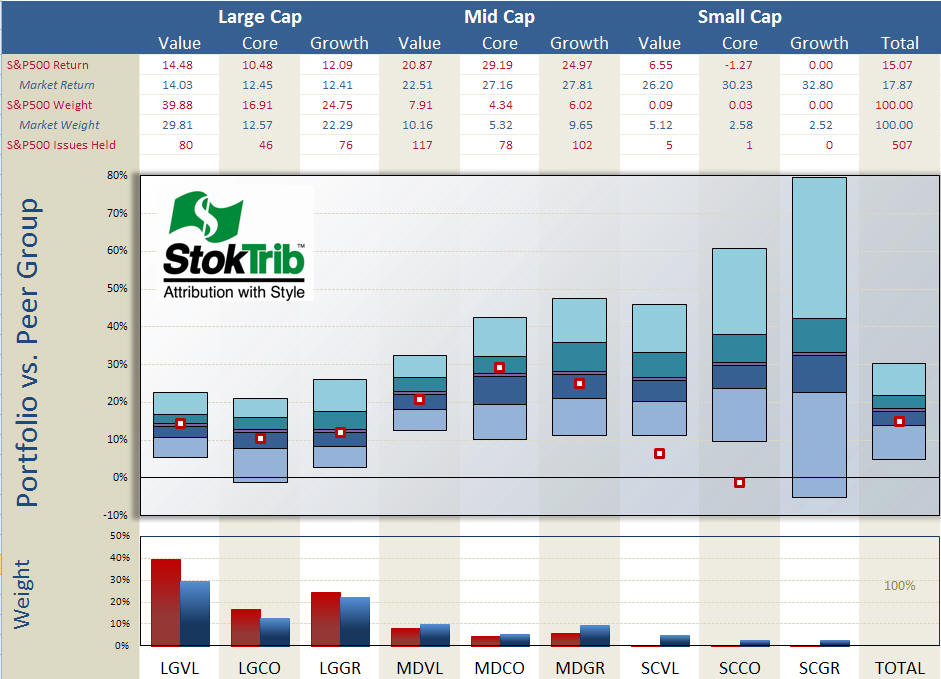

We begin with an analysis of the style composition and performance of the S&P500 as shown in the next exhibit.

The portfolio in the exhibit is the S&P500 index and the benchmark is the entire U.S. stock market, as provided by Compustat. Let's begin with a discussion of the style make-up of the S&P as shown in the bottom of the graph. Unsurprisingly, the S&P has a large-company orientation, especially tilted toward large-value companies. The total market is about 30% large-cap value, whereas the S&P is 40% large-cap value. Throughout this commentary I use Surz Style Pure® indexes defined at Style Definitions.

This large-company orientation hurt the S&P because smaller companies performed better in the year, as shown by the middles of the floating bars in the center graph. These floating bars represent pure scientific peer groups described at Portfolio Opportunity Distributions (PODs). The median of each POD is the return for that style in aggregate and the ranges are the return opportunities for that style. As you can see, smaller companies returned in excess of 25%, with small-cap growth leading the way with a 33% return, while larger companies lagged with returns in the low teens. Large-cap value in particular returned 14%. It was primarily this concentration in large-value companies that caused the S&P (15%) to lag the total market (18%) in 2010, as shown in the far right table and floating bar. In other words, allocation to styles penalized the S&P relative to the total market in 2010. The other component of attribution is stock selection, which we can see as the location of the dots in the exhibit. For the most part, the stocks selected by the S&P committee performed near their respective medians within each style, with the exception of smaller companies which don't matter much because the allocations were minimal.

You can use this exhibit to rank individual managers within styles, as well as rank their style components. Just plot your dots in the graph above. For example, locate your manager's style in the exhibit (large value, small growth, etc.), and place his rate of return within the corresponding floating bar, using the scale on the left and the median from the table above as your guide. Voila, an accurate ranking.

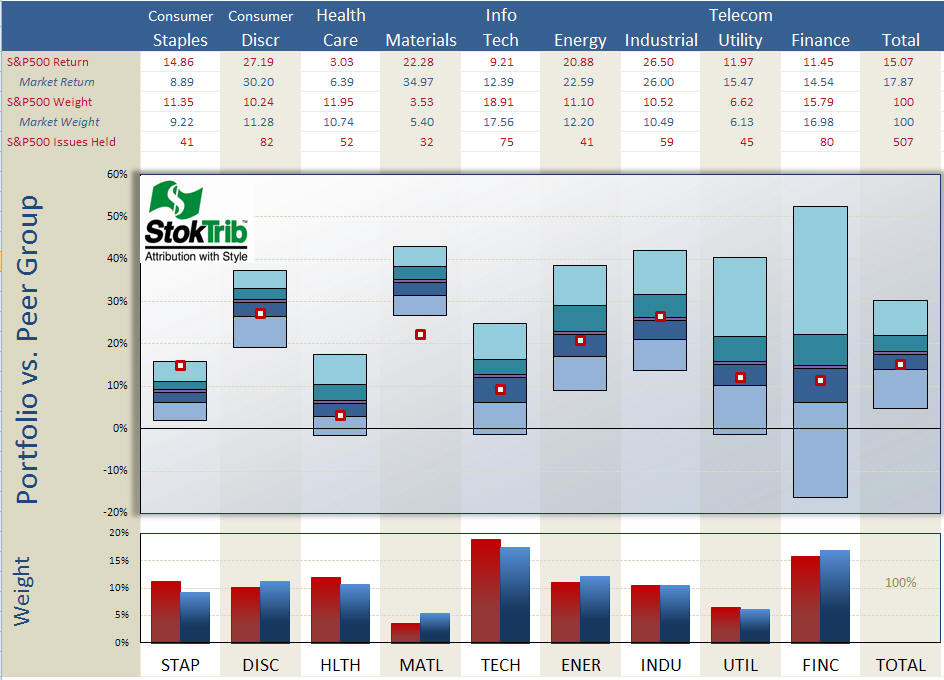

Next, I performed a similar analysis, decomposing the S&P by economic sector, and concluded that stock selection hurt performance. But how can that be in light of what I just concluded in the previous paragraph where stock selection was not a factor? Sector allocations of the S&P are in line with those of the total market, mainly because the S&P is a large part of the total market. What we're seeing in the next exhibit are the style impacts on performance within economic sectors: style effects manifest themselves as stock selection when the S&P is decomposed by sector. The lesson to be learned here in our odyssey is that we need to be careful to evaluate skill rather than style. An attribution against the S&P500 by sector can be easy in some sectors and difficult in others if the S&P is not the correct benchmark. For example, a manager with a broadly diversified portfolio will have a return on Materials that is something like the 34.97% shown for the total market in the table below. This is 13% greater than the S&P's 22.28% return in Materials, which would appear to be a big success, and it would be a big success if the S&P were the correct benchmark, but in this hypothetical we've said that the manager is more broadly diversified than the S&P, so the outperformance is most likely caused by style (broadly diversified) rather than good stock picking.

The performance attribution puzzle is complicated, but well worth the time and effort to get it right. Because it tells us why performance is good or bad, attribution is a window into the future. We want confidence in the manager's strengths, and comfort that failures are being addressed and corrected.

Follow the "dancing balls" in the exhibit above. The S&P's only "success" (i.e., performance above the median of the broad market) was in Consumer Staples. It lagged in every other sector, especially Materials, although that allocation was small. The most harmful shortcomings are in Technology and Financials because of the significant weights. Note also the middles of the floating bars; Consumer Discretionary and Materials performed best in the year while Healthcare and Consumer Staples performed worst. And also note the ranges of the bars, with Financials exhibiting a wide range of opportunities, reflecting the volatility within that segment of the market; where there's risk there's opportunity.

In addition to this attribution, it's helpful to understand performance at the individual stock level as shown in the following "Biggest, Best, Worst" exhibit

Here are some observations from this table. Exxon Mobil was the largest holding in the S&P, representing over 3% of the index on average in 2010. The top 10 holdings comprise 18.84% of the index, reflecting concentration in this 500 stock portfolio because an equal weighting would have just 2% in the top 10. As indicated by the red highlights, four of the top 10 holdings were the biggest contributors (largest positive "Impact", defined as return times commitment) for the year, and one of the top 10 was among the largest detractors; these are likely to be the same winners and losers that you'll find in your large-cap managers' portfolios. The "effective returns" for these holdings are close to their "report-period returns," indicating relatively constant weights throughout the year. "Effective return" is a performance attribution breakthrough described at Effective Return Article. It measures the allocation-weighted return on a stock, and therefore captures the combined effects of stock performance and manager allocation decisions. Effective return is larger than the traditional holding period return if allocations are advantageous, holding more of the stock when performance is good than when it is bad. Of course the reverse is true if allocations are disadvantageous.

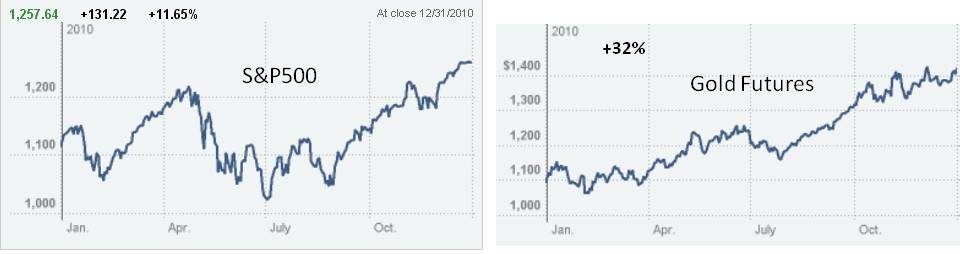

We dodged a bullet in 2010. At mid-year it was looking like 2010 was going to be a big fat letdown, but the last half of the year brought a nice recovery. In the meantime, gold, a current hot topic, continued its upward progression throughout the year. Gold was less volatile than U.S. stocks. (Graphs courtesy of the New York Times)

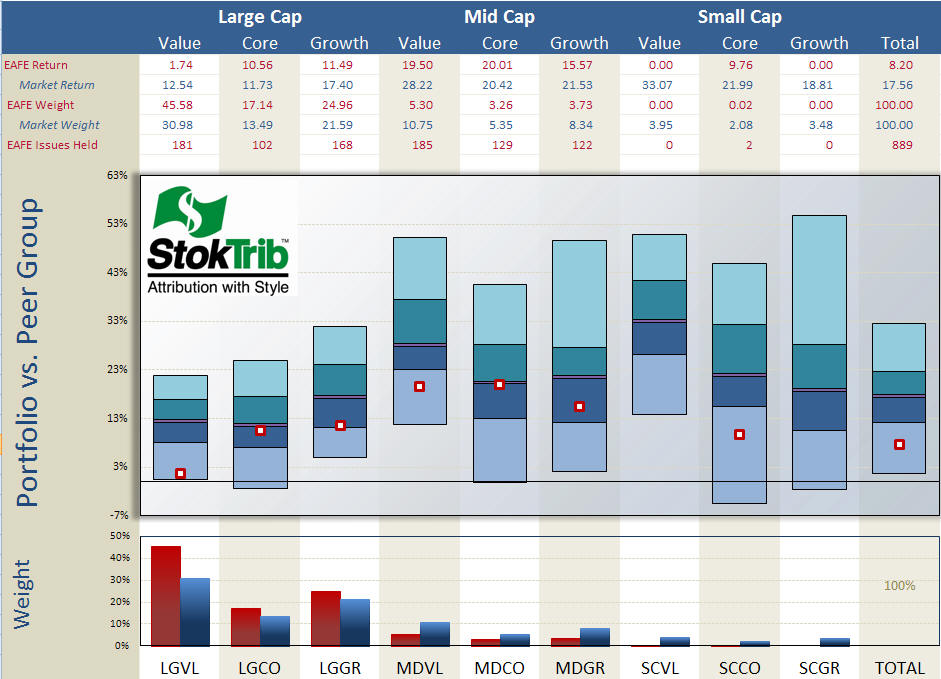

Non-US Stock Market

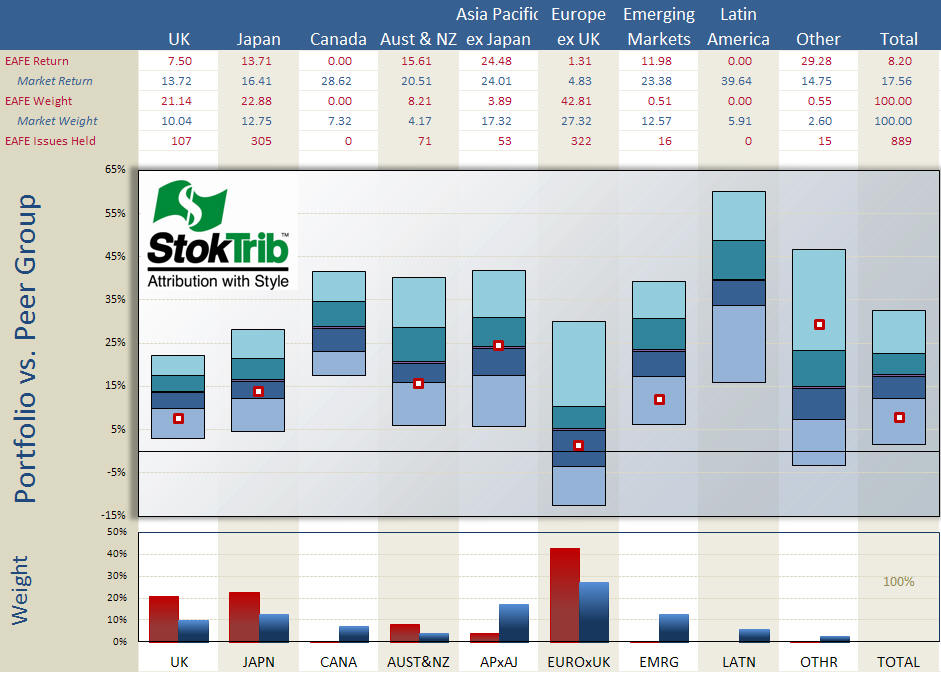

Now let's turn our attention outside the US, where the total foreign market earned 17.5%, in line with the total US market's 18%, but the Europe Australia and Far East (EAFE) index substantially lagged the total foreign market, earning only 8%. The following exhibit shows that, like the S&P, the EAFE index is large-company oriented, and this orientation was not in favor. Small-to-mid ("Smid") cap value was in favor outside the US. However, unlike the S&P, stock selection within styles was poor. This is due to the country allocations of the EAFE. In other words, the EAFE suffered a double whammy: both style and country allocations were out of favor in 2010. The EAFE's large value orientation was out of favor, as was its overweight in Europe-ex-UK, and its absence from Latin America. Like the U.S. graph, this graph can be used to rank your foreign managers.

As shown in the following exhibit, Europe-ex-UK was the worst performing region, and EAFE was overweight this region. The index was also void the best performing Latin America region.

In summary, the performance of the EAFE index can be decomposed as follows:

EAFE performance in 2010

|

Total Market: |

17.6% |

|

EAFE large company orientation: |

-3.1% |

|

EAFE country composition: |

-6.3% |

|

EAFE Return: |

8.2% |

The 85-Year History of the U.S. Capital Markets

The following histograms show the history of risk and return for stocks (S&P500) and bonds (Citigroup High Grade). There are many lessons in these graphs, so it's worth your time and effort to review these results.

This Website Is For Financial Professionals Only