Stoic Stocks

The problem is that Greece isn't hitting its targets, Greek bond yields have surged to 16%, and another bailout and debt restructuring (soft form of default) are both inevitable. Foreign (mostly French and German) banks hold $110 billion of Greek debt that, if officially in default, would require them to raise capital – a painful hit but a manageable crisis. Where it gets dicey, however, is if you assume that a collapse of confidence spreads to Irish, Portuguese and Spanish debt. Altogether, foreign banks hold $1.1 trillion of these four PIGS' sovereign debt. The ECB, IMF and European governments need to insure that a stampede away from these credits doesn't get started – and that's where the market jitters are coming from. Can they contain it? So far, markets are betting they can. That's the Greek crisis. Then there's the U.S.'s debt ceiling, softer economic data, China and India further tightening credit and Middle East turmoil. Add it all up and the Wall of Worry isn't showing many cracks.

And yet, stocks have been taking the punches mighty stoically. The S&P 500 is off just -3% from its April 29th peak. By contrast, last year's Greece-inspired May/June selloff racked up to -16%. Maybe more downside is in store this summer; but I think, looking at U.S. fundamentals, that stocks are acting rationally in holding up as well as they have. Let's go through some of the latest data.

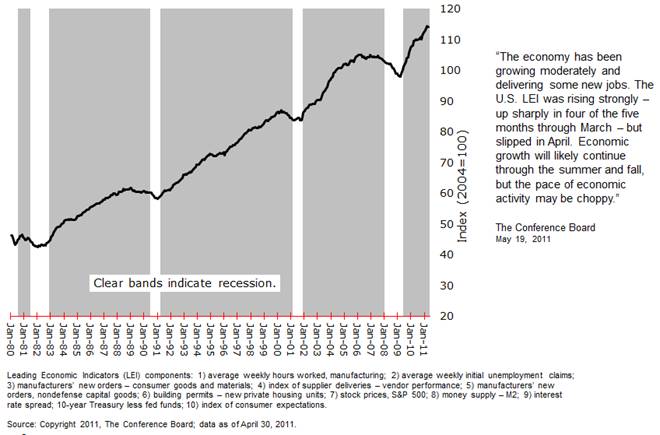

April's index of leading economic indicators ticked down for the first time in six months but the Conference Board interpreted this number benignly: growth will continue but it may be choppy for a while. In this chart, note last summer's very evident pause in the series followed by a resumption upward. I wanted to show you this chart because history suggests the LEI has to really roll over before you get too concerned about a material, sustained slowdown.

Index of Leading Economic Indicators

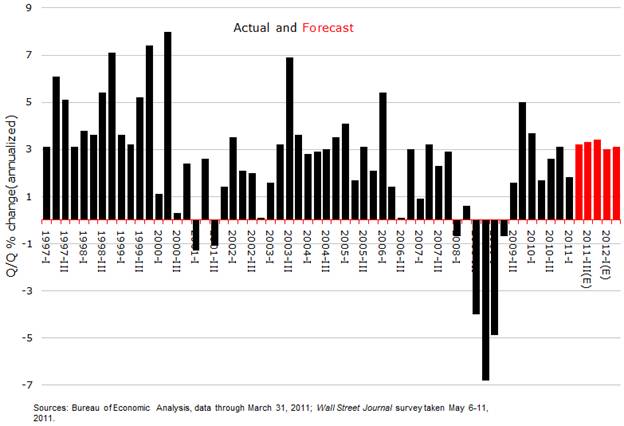

The 55 best and brightest economists just surveyed by the Wall Street Journal also on average concluded that the first quarter's soft patch will likely resolve into a re-acceleration of economic growth later in the year. See the red bars in the chart, below. While a shortage of car parts related to Japan's reactor meltdown is indeed dampening manufacturing, car production is expected to snap back strongly later in the year as final demand has been strong and auto inventories are being depleted.

Quarterly GDP Growth (annualized)

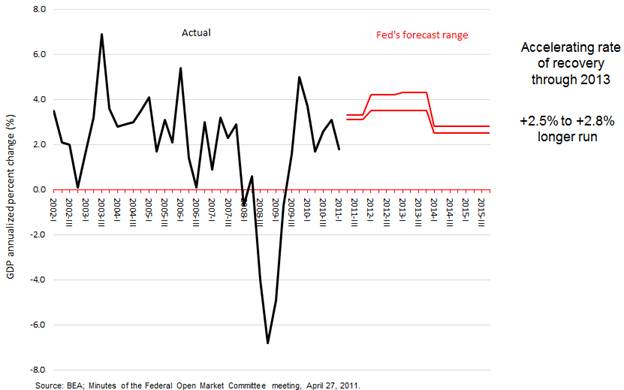

Finally, with last week's release by the FOMC of their April 26-27 meeting notes it's interesting to note the Fed's reading of the economic outlook in the chart, below. They reported that several committee members “indicated that, in contrast to the somewhat weaker recent economic data, their business contacts were more positive about the economy's prospects, which supported the participants' view that the recent weakness was likely to prove temporary.”

Quarterly GDP Growth (annualized)

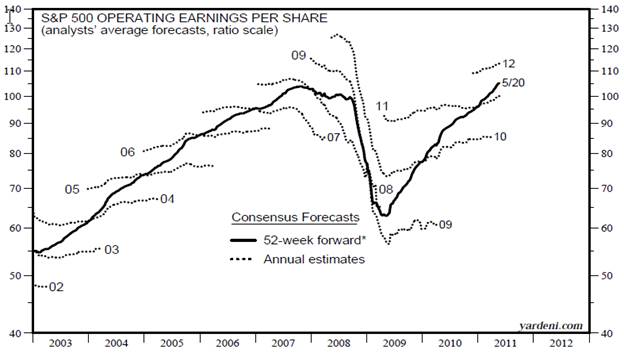

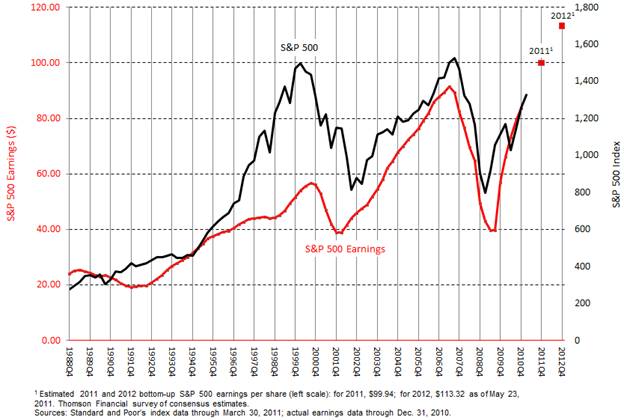

Wall Street analysts are coming to the same conclusion – that despite the possibility of near-term slower economic growth, 2011 corporate earnings will likely post another very sizeable jump over 2010, and likewise for 2012. In fact, the bottom-up consensus estimate for 2011 S&P 500 earnings has undergone steady upward revision, as Yardeni Research shows with the dotted lines in the following chart.

Plotting today's S&P 500 earnings estimates against the Index results in the following chart. If we come anywhere close to the forecasted ~$100 per share in earnings this year, I have to believe the Index will end the year a good deal higher than at 1320 where it closed today. Most Wall Street strategists have year-end targets between 1400 and 1500, for which this chart provides such a clear rationale. A reasonable market P/E ratio of 15 applied to $100 in earnings would put the index at 1500.

S&P 500 Index and Earnings

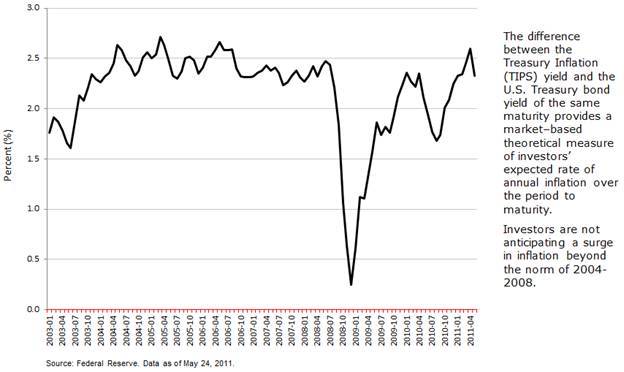

The Greek debt crisis, China's ongoing efforts to brake economic growth and break inflation and the global manufacturing slowdown related to auto parts shortages have all conspired to ratchet down U.S. inflation expectations, knock commodity prices out of their recent speculative orbit, and bolster the U.S. dollar. In the following chart you can see in the TIPS spread – the best market-based measure of 10-year inflation expectations – the market's complacency over inflation prospects.

TIPS Spread Measure of Expected Inflation

The debate over the commodities outlook rages on CNBC, I've noticed. My own opinion is that the global expansion will continue and as it pertains to commodities, the China-India-Brazil expansion story will continue, so that any retracement in the price of copper and crude oil, for example, will prove temporary.

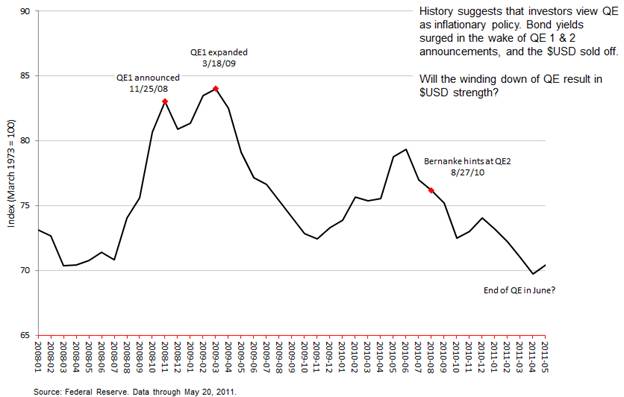

Because commodities prices have had a strong inverse correlation to the U.S. dollar one might expect that if copper and crude are weak for a stretch, then the dollar should strengthen for a stretch – both of which I think make sense. Another reason to expect near-term dollar strength is in the following chart, which shows how QE has been associated with dollar weakness – so the end of QE might also mean dollar strength.

U.S. Dollar - Major Currencies Index

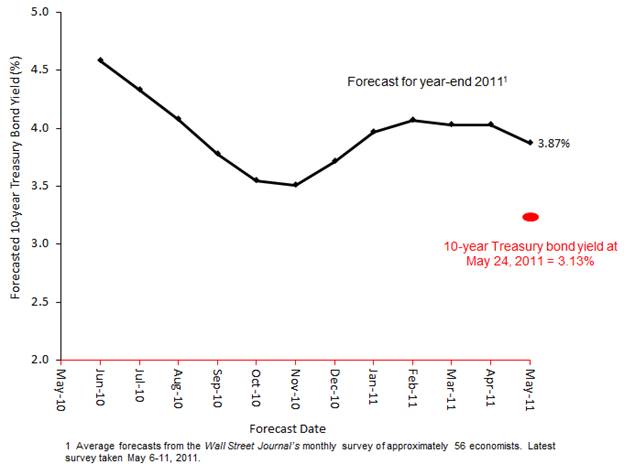

Similarly, investors have bid up bond prices driving yields lower in anticipation of the end of QE. That's been exactly counter to what had been generally assumed – that yields would rise as the Fed backed away from being a big Treasury buyer. It's happening because investors view QE as inflationary policy so its demise might be deflationary. With this in mind, I think that bond yields could stay lower than (almost) anybody had thought likely, and the experts' bond yield forecasts could very well continue along the downward course that has already begun, as you can see in the following chart.

10-year Treasury Bond Yield Forecast

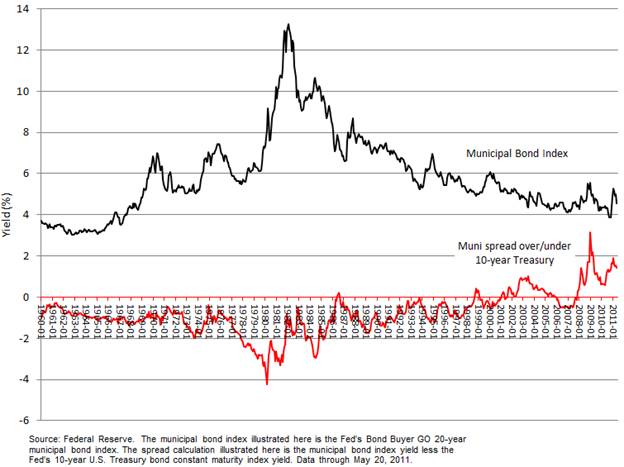

Speaking of bond yields what about munis? I think they're still on sale despite some recent upward price movement. I say this based on the following chart showing the muni index yield's spread to the 10-year Treasury yield.

Meredith Whitney and Nouriel Roubini have been vocal about how we'll likely experience an unprecedented surge in muni defaults. That doesn't seem reasonable given the improvement we've already seen in municipal finances. See the chart, below. Sure, there could be some high-profile blowups but, if you do your homework on individual issues, or hire a good manager to do it, I think you can find real value in munis.

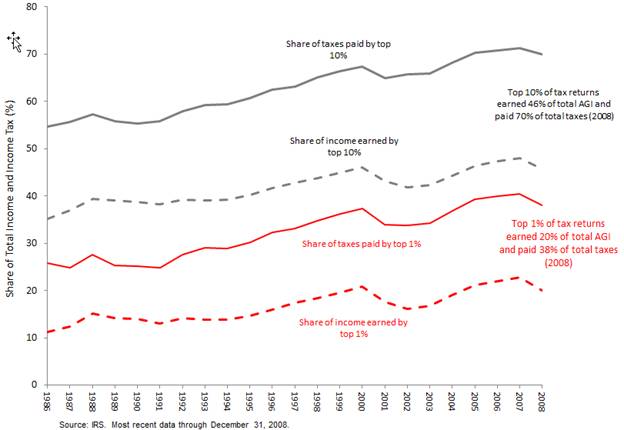

I'll wrap up this month's notes with a comment on taxes, as that subject will be in the headlines as long as the U.S. deficit and debt crisis remains unresolved. What brings this to mind was Tim Geithner's speech last week in which he once again referred to the administration's position that the tax code should be more “fair” … so taxes on the highest earners should go back up to pre-Bush tax cut rates. Today the top 1% of earners account for 20% of total adjusted gross income (AGI) and pay 38% of total income taxes. The top 10% earn 46% of total AGI and pay 70% of total income taxes. The share of both AGI and total taxes paid by the highest earners has risen steadily over recent decades and the proportion of one to the other, if anything, has become slightly more progressive. See the following chart. I just want to get this data in front of you because I think the moral argument against more "fairness" is a good one: why should the system be made any more progressive than it currently is, particularly when the bottom 50% of earners pay no income taxes? Also, the data suggest to me that the system is no less fair today than it was in 1986. You decide. “Fairness” is definitely in the eye of the beholder.

Shares of Federal AGI and Income Taxes Paid

This Website Is For Financial Professionals Only