IMCA Sets Out To Define “Wealth Management” But Critics And Competitors Take Issue With The Definition Hot

“This job analysis clearly defines wealth management as a distinct practice of advising high-net-worth clients with specialized expertise and skills,” Sean R. Walters, CAE, executive director and CEO at IMCA said in a release “Financial advisors without this knowledge who work with affluent clients are doing them a disservice.”

Highlights from IMCA’s wealth management job analysis and the executive summary white paper, “Defining Wealth Management, Serving High-Net-Worth Clients with a Distinct Body of Knowledge,” include the following:

- Wealth management is a distinct practice. Advanced competency in this discipline may be practiced by financial planners, accountants, estate planning attorneys, or investment professionals.

- $5 million is the minimum net worth a client must possess to be considered a high-net-worth client.

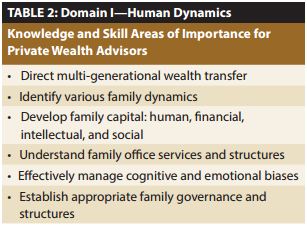

- The knowledge required to provide competent wealth management incorporates 169 topics within four knowledge domains: human dynamics, wealth management strategies, client specialization, and legacy planning.

- The fundamental tasks and the process that private wealth advisors use in working with clients may be similar to financial planning—and many other client-oriented professions—but an advanced and unique set of knowledge and skills is needed to effectively serve high-net-worth clients

Advisers, meanwhile, had mixed reaction to IMCA’s definition of wealth management.

Some IMCA members expressed full support. “I am in complete agreement with Sean Walters and the findings of the study,” says Brian Ullsperger, CIMA, AIF of WTAS LLC. “I am of the strong belief that true wealth management is a comprehensive, integrated and ongoing process that blends investment, tax and estate planning into a cohesive strategy to achieve an individual’s or more often a family's goals over multiple generations. This requires a broad array of skills and ongoing training. The CPWA certification provides the foundation for an advisor to develop the knowledge required to build a wealth management practice.”

Richard Rosso, MS, CFP, CIMA, a senior financial advisor with Clarityfinancial, also expressed support."There needs to be a clearer definition, or path to understanding the needs of the wealthy and IMCA in my opinion, is well-equipped to forge the way," he says. "I believe increasing external change will affect this segment more than any other group going forward, especially on the tax and legacy-planning front so this structure will be necessary."

What's more, Rosso said IMCA will be able to further identify and clarify the process of advising the wealthy. "Segmenting into the four knowledge domains will be very effective," he says. "Understanding the human dynamics of the wealthy and their families and to sharpen the skills needed to spur dialogue among family members will be crucial guidance required by today’s advisor. Enhanced EQ skills will be required."

For his part, Rosso says he does financial planning “plus,” for affluent investors. "You begin with the basics and then move into areas of specialization like stock option exercise strategies, legacy/gifting implementation, retirement income withdrawal maximization and the unique behavioral threads that tie all this together," he says. "For IMCA to create a formal direction with a robust body of knowledge would be welcomed."

Meanwhile, others say IMCA's findings are convenient and self-serving.

“It appears to me that IMCA has conveniently drawn the line of what makes a high-net worth client at the point of the current estate tax exemption,” says Chris Lipper, CFP, CIMA, president and chief investment officer at CPF Texas.

“If the exemption drops to $3.5 million or $1 million next year, will that be the new point of demarcation?” ask Lipper, who for the record holds the other designation administered by IMCA, the CIMA.

Lipper agrees that estate and legacy planning requires a higher level of competency. “However, as a CFP certificant, and more importantly, with almost 18 years of experience working with high net worth clients, I have the expertise,” Lipper says. “Holding the CPWA designation does not bring instant qualification, nor do those without the designation lack expertise.”

Others also took issue with IMCA’s findings.

For instance, Stephen Horan, Ph.D., CFA, CIPM, who is head of university relations and private wealth at CFA Institute, says the study’s methodology and interpretation are curious. “The process of removing advisors with clients less than $1 million and then concluding from the analysis that wealth management is the practice of serving clients with more than $5 million is tautological,” Horan says. “The investigator effective determines their conclusion by the design of the study. Despite the design bias, fully a third of respondents, put the minimum below $5 million.”

Horan also says the origin of the 43,000 financial professionals to whom the survey was sent is unclear. “So, it is difficult to interpret the results without understanding the characteristics of the population to whom the survey was sent,” Horan says.

Plus, Horan notes that the 400 responses, which was filtered down to 250, represent a response rate of less than 1% and weaken the validity of the report’s conclusions.

And Horan says the firm-type of the respondents does not reflect the industry. “It is heavily weighted toward brokerage and private banks and less on independent RIAs, which are growing in significance,” he says.

Horan also says the comparative analysis in Tables 1 and 2 (see below) list topics in the CPWA not covered in other most other programs, but does not list those programs. “The CFA program was apparently not included because it, for example, covers tax-aware investing, asset-protection strategies, advance stock option planning and strategies, endowments and foundations, and legacy planning,” Horan says.

Says Horan: “I’ve performed a detailed comparative analysis of the CPWA program with other credentials. The CPWA has no coverage of economics, financial statement analysis, equity valuation, or fixed income valuation according to its website. Its coverage of derivatives is cursory compared to the CFA program.”

By way of background, the CFA Program – according to its website – is a “globally recognized, graduate-level curriculum that provides a strong foundation of real-world investment analysis and portfolio management skills along with the practical knowledge you need in today’s investment industry.”

In sum, Horan says IMCA’s study does help focus attention on the complexity and diversify of wealth management, but it is ultimately “ill-designed, superficial, erroneous, and self-serving.”

For its part, IMCA said in its release that, in addition to clarifying what constitutes a private wealth advisor, it will use the analysis to refine the experience, education, examination, and ethics requirements of its CPWA certification program. The organization, who members collectively manage more than $1.6 trillion on behalf of 1.3 million clients, has administered the CPWA certification since 2007, and the program was operated as a certificate program since 2004.

IMCA said in its release that the procedures used in the job analysis study complied with all relevant technical and legal standards for professional certification and licensure as well as the requirements for accreditation by the National Commission for Certifying Agencies (NCCA) and the American National Standards Institute (ANSI).

In response to critics, Walters said IMCA didn’t conduct the analysis to be self-serving. "We facilitated a process to codify the body of knowledge and skills necessary for competent performance of “wealth management” as defined by practitioners in the field," he says. "The job analysis process is a best practice for certifications, and a requirement to be accredited under ALL third-party personnel certification standards. Every valid certification body, regardless of industry, defines the body of knowledge required for a certification using this process. When a designation program purports to define a body of knowledge using the intellectual property of an individual or a handful of academics, it is not a legitimate certification program and should not be treated as such.”

By way of history, the financial planning industry has for years been trying to define financial planning with some success. In 2011, after two years of work, major firms affiliated with the FPA developed this definition: “Financial planning is the process of developing a strategy or program to assist in the achievement of at least one financial goal or need. The process starts by gathering and analyzing relevant financial data, client values and goals, and it results in an action plan or recommendations, including acknowledgement of other financial issues that may deserve attention.”

This Website Is For Financial Professionals Only

NAPFA Must Do The Right Thing With CPA/PFSs If It Wants To Retain Its Special Role As An Advocate For Consumers

NAPFA Must Do The Right Thing With CPA/PFSs If It Wants To Retain Its Special Role As An Advocate For Consumers CFA Level 1 Exam Prep Now Being Offered By The American College, Reflecting The Growing Popularity Of The CFA Designation

CFA Level 1 Exam Prep Now Being Offered By The American College, Reflecting The Growing Popularity Of The CFA Designation Charles J. Yang, CFA, Elected Chair Of CFA Institute Board Of Governors

Charles J. Yang, CFA, Elected Chair Of CFA Institute Board Of Governors NAPFA, In Saying Only CFPs Can Become Members, Snubbed The AICPA, Exposing Fractures In The Movement To Professionalize

NAPFA, In Saying Only CFPs Can Become Members, Snubbed The AICPA, Exposing Fractures In The Movement To Professionalize