Showing Clients How Dividend Paying Stocks Can Help Offset Low Interest Rates

Low interest rates have been a serious problem for those approaching retirement and in retirement. Many people thought that they could simply plunk most of the investments into laddered treasury bonds when they retire and live off the income. But with the ten year Treasury bond barely yielding 2% and consumer price inflation running at 3%, this strategy is no longer viable for a lot of people.

There are several ways for advisors to help clients overcome the problem of low interest rates today. In this article I want to focus on getting clients to move some of their money into dividend paying stocks that have a solid dividend yield, are not too cyclical with economic growth, and have shown consistent dividend growth over time.

Let’s look at one such company: Johnson & Johnson (JNJ). Johnson & Johnson currently has a dividend yield of 3.5%, has seen its dividend grow by about 9% annually over the past five years, and they have never failed to increase their dividend on an annual basis since paying their first dividend in 1970.

Let’s compare what types of returns we might expect to see for JNJ vs. a 10 year treasury bond. I ran a total return analysis on JNJ using our free dividend calculator called Total Returns- Dividend vs. Price Appreciation. In the outputs below I assumed a ten year holding period for both investments. I also assumed that the dividend for JNJ grows by 6% per year and, to be conservative, that the stock price doesn’t move.

|

Total Return |

Annual Return |

|

|

10 Year Treasury |

21.9% |

2.0% |

|

Johnson & Johnson |

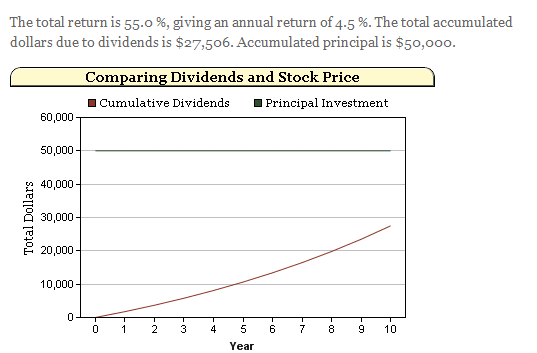

55.0% |

4.5% |

Johnson & Johnson Dividend Analysis (assumes $50K invested and no stock price growth):

Over the ten year holding period in this scenario, JNJ would return nearly 35% more than the ten year Treasury bond.

Let’s look at this another way: How much does it mean to a client’s retirement plan if he is 100% invested in fixed income and he moves half of this money to dividend paying stocks such as Johnson & Johnson? I looked at a plan in our retirement planner where a couple will retire in 5 years at age 65. They have $400,000 saved and all of it is in fixed income returning 2%. They will also receive $25,000 in social security payments starting at age 65 and they have $40,000 in expenses per year.

Under this scenario their funds will run out when they are 89 years old. But what if we move half of their money to dividend paying stocks that return 4.5%? In this case they would not run out of money until age 98, a difference of 9 years.

My goal here is not to get all clients to jump back into the stock market with both feet. But there is a place in many retirement portfolios for mature companies that have shown that they will increase their dividends over time. By showing clients results like I’ve presented today, it might help convince them that they are in fact better off with at least some of their investments in dividend paying stocks as opposed to having everything in treasury bonds.

This Website Is For Financial Professionals Only