Don't Panic

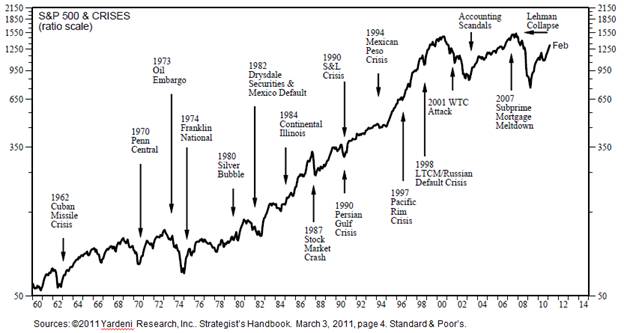

On all three of these issues visibility is extremely hazy and not likely to come clear overnight. The S&P 500 is off -6% from its February high, having run up +28% almost in a straight line from the August bottom which, in itself, suggested a pretty high probability of a correction. Recall that last summer’s plunge totaled -17% from peak to trough and stocks churned for four months before regaining traction. That might not be a bad template to keep in mind for this year, which is to say that I won’t be surprised if the present market situation gets worse and lasts awhile before much optimism seeps back in. One talking head on CNBC just told the viewers to be prepared for a 1000 point drop on the Dow! Not surprising, I guess, as crises always bring the bears crawling from the woodwork. Actually, while that sounds scary, a 1000 point drop on the Dow would put the index down another -8% and back on its 200-day moving average – not that big a deal in the big scheme of the stock market. My own view is that you sit tight and ride out this year’s crises, just as it made sense to do so last year. I’m not a trader. I’m an investor. I think most great investors, like Warren Buffet, probably carry this chart around in their heads, which is the single best piece of advice I can give in times like these.

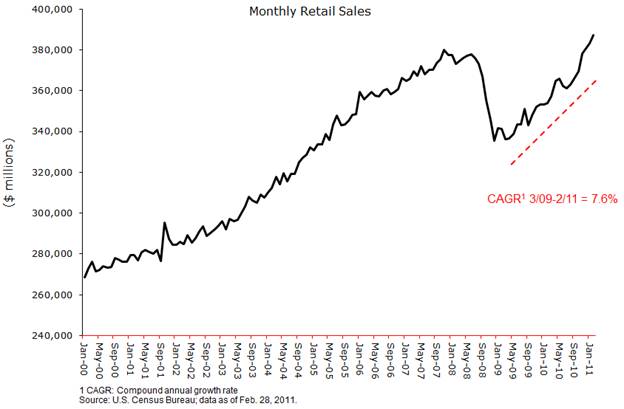

One of the most significant of the month’s new economic data was February retail sales, which again demonstrated how Americans have come flocking back to the stores – and to Amazon. As we all know, consumers account for 70% of the GDP and it is they who must drive the economic recovery. Well, they’re doing it and, I think, will continue to do it. Retail sales have gone out to new all-time highs and the rate of retail sales growth has accelerated in recent months. Gradually improving jobs data will likely extend this trend.

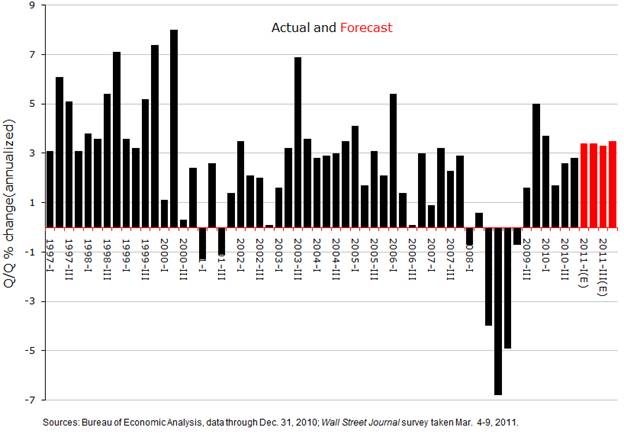

Most economists say they’re not inclined to chop their GDP growth forecasts unless and until crude oil prices hit the $125/bbl neighborhood and appear likely to stay there for a while. That hasn’t happened and, if we can believe the Saudis, is not likely to happen. Obviously, there’s much risk around any oil price forecast but, for now, I think it’s an OK assumption. So, the very latest consensus GDP growth forecast from the 50 economists polled by The Wall Street Journal each month is what you see in the following chart. The bottom line is that economists are still firmly in the recovery-has-legs camp, despite the many concerns we’re all familiar with.

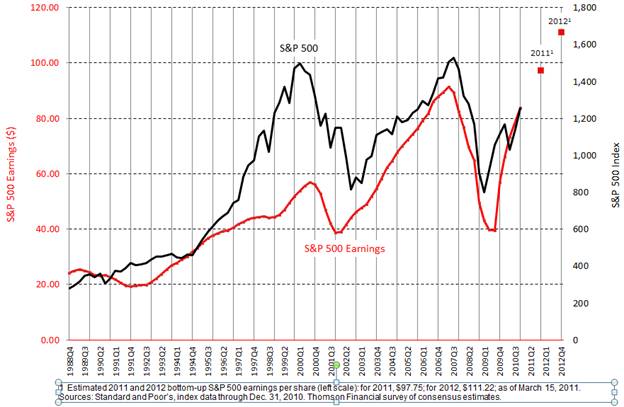

GDP is a measure of the economy’s top line, total sales. Sales drive earnings, earnings drive stock prices. If the economic recovery does continue to unfold as economists expect, then earnings are headed much higher. How much higher and what does this mean for stock prices? The numbers are illustrated in the following chart. Interestingly, despite all of the last month’s problems, analysts actually bumped their S&P 500 earnings estimates higher, again. Which is to say the feet on the street who daily talk to company managements haven’t yet wavered in their strong earnings recovery convictions. When I look at this chart I ask myself “if the red line (earnings) goes higher, what is the black line (stock prices) likely to do between now and the end of the year?” You get the picture. This chart so clearly illustrates why most Wall Street strategists have pegged their year-end targets for the S&P 500 at 1450, or thereabouts. Goldman Sachs is at 1500. While it may seem like pie-in-the-sky in the present crisis atmosphere, it does make perfect sense. Those targets assume a year-end market P/E multiple on trailing earnings of 15 times – not a stretch, in fact, very reasonable by historic comparison.

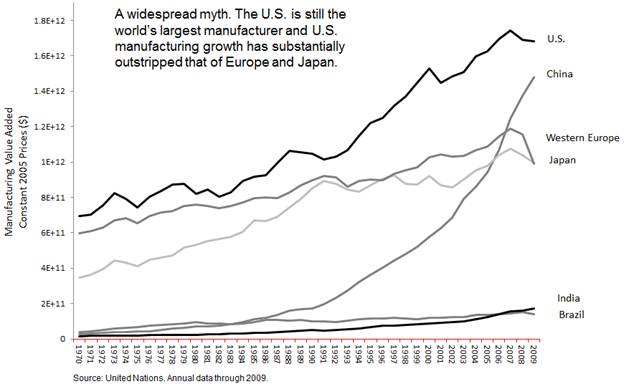

Just one last point on a slightly different topic, since I happened to be working on the numbers this month. We’ve all heard that “the U.S. doesn’t manufacture anything anymore.” The sub-text of this whining complaint is that our country is going down the drain, that a service economy is qualitatively inferior to a manufacturing economy, that our standard of living is headed inexorably lower. As a matter of fact, none of this is true. I can address the service-economy topic in future installments, but what about that first point – that we don’t manufacture anything anymore? Take a look at the following chart. It turns out that U.S. manufacturing might has remained extraordinary. Yes, of course China has made huge gains, which is what you would have to expect from the unleashing into a market economy of 1.3 billion under-productively employed people compared to the U.S.’s 310 million. But, the fact is that the U.S. is still the world’s largest manufacturer and manufacturing growth over the last three decades has accelerated from the three decades prior to 1980.

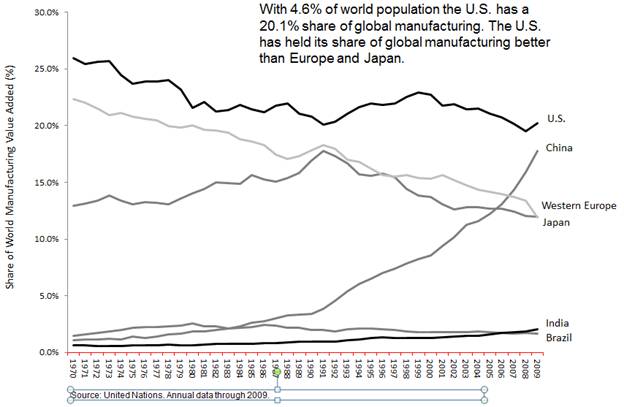

The related statistic is that the U.S. has actually held on to virtually all of its global share of manufacturing, even as Europe and Japan really have been going down the drain on this measure.

What Americans see, however, is that manufacturing jobs, at about 9% of total U.S. jobs, have declined from 38% at the end of WWII, taken to be a bad thing. With extraordinary gains in productivity over the last six decades we can make much more stuff with fewer and fewer people, freeing up those people to work in services. The largest and fastest growing jobs category of all is health care and education, in which wages are, on average, substantially higher than production jobs. Did you know that, according to the Bureau of Labor Statistics, teachers, on average, make over $50/hour compared to the average for production workers of $25/hour? Similar for health care workers and many of the other service job categories. I make these important points because this topic – the “decline” of American manufacturing – is so often trotted out as a reason to be pessimistic about our economic future. Truly an unfortunate but widespread myth.

This Website Is For Financial Professionals Only