What Investors Are Overlooking About Interest Rates

FOMC is projecting a historically gradual pace of increases

The FOMCs’ most recent forecasts have them increasing policy rates four times in 2016 – or about 100 bps. If in fact the Fed were to raise rates just four times in 2016, it would mark the slowest rate of increase for a tightening cycle in its history!

What is the market’s view?

Financial markets have an even more benign outlook for future increases in interest rates! Futures are pricing in little more than two rate increases in 2016 – a meager 50bps. How can this be? Markets seem to be pricing in an unusually high risk of deflation in the near future. One recent dealer report on measures of inflation expectations estimated that financial markets had priced in a one in three chance of inflation remaining below 1% percent for the next five years.

Investors should be skeptical about how gradual this cycle will play out

Investors should be highly skeptical of the market’s view of inflation and their extremely shallow path of rates. Certainly inflation is subdued today, but that is very different from expecting deflation to be a major threat going forward. You don’t need to be an inflation hawk to find such a scenario overly gloomy!

Despite current near-zero headline inflation readings, there are several strong signals that inflation and interest rates are poised to move higher in 2016 and surprise to the upside:

The FOMC’s intention is not a commitment

The Fed’s preference for a gradual pace of future rate hikes should not be construed as a commitment on their part. That is, no matter how strong their intention may be, it is still highly conditional. The FOMC included language in their December statement to indicate that the actual pace will depend on how the economy performs:

“The actual path of the funds rate will depend on the economic outlook as informed by incoming data

Inflation will surprise to the upside in 2016

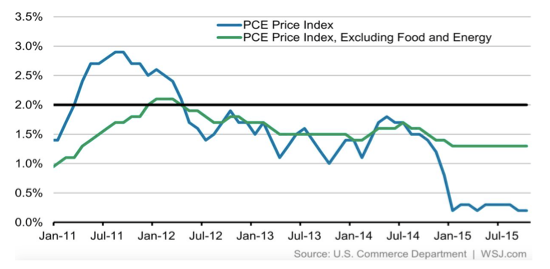

Headline inflation has stabilized and is poised to move higher

Measures of headline inflation plunged after the nosedive in commodities prices late last year. More recently, however, they have arrested their steep decline. Now that it has stabilized, headline inflation is poised to move higher over the next few months. The base effects from last year’s plunge in commodity will roll off completely by early 2016 and buoy annual measures of inflation.

Some measures of core inflation actually increased in 2015

Though it is not the Fed’s preferred measure of inflation, core CPI has grown steadily throughout 2015. It started the year at 1.6% and in November, it reached 2% - the Fed’s inflation objective. Look for headline inflation to converge with core inflation as the year goes on.

Wages are another potential catalyst for inflation

Job growth has been very strong the last two years and the unemployment rate has fallen to 5.0% - it’s lowest level since early 2008. By many estimates, this is at or very near the full employment rate. In other words, the unemployment rate cannot continue to grind lower from its very low level without sparking wage growth and inflation.

Recent wage data supports this view as well. Average hourly earnings of private sector employees were up 2.5 percent on an annual basis – the largest increase in more than six years. Furthermore, inflation-adjusted hourly compensation grew by 3.4 percent in the third quarter of 2015, marking the second-largest jump since 2009.

The prominent German economist Rudi Dornbusch used to say, “In economics, things will take longer to happen than you think they will, and then they happen faster than you thought they could.”

This may well be the case for rising inflation and interest rates in 2016.

This Website Is For Financial Professionals Only