What you’re saying looks great. But what about the US government simply not dealing with the mountain of debt?

Right. And dealing with the debt problem is a key caveat to having a long-term positive view of the U.S. economy and markets.

But, I think we’ll get there. Why? Because the debt problem is solvable in a way that, I think, will in the end be acceptable to most Americans.

In its simplest terms, the solution amounts to taking the rate of growth in entitlement spending down from its current estimated 5-1/2%/year through 2023, to a rate that’s in line with nominal GDP growth – currently estimated by CBO at 4-3/4%/year. That’s not a “cut”. It’s a cut in the rate of growth. And, not even remotely draconian. That’s why I think we’ll get there.

About corporations claiming that they keep money out of the US because our tax rates are high (slide 23). How do we rate when comparing corporate tax rates?

U.S. corporations are subject to a 35% maximum income tax rate – the highest in the world. However, the effective marginal tax rate, is only 26% due to deductions and preferences. U.S. corporations are taxed on foreign earnings when they repatriate the cash – that’s on top of foreign income taxes already paid. Hence, companies’ not repatriating their earnings. See this article for a good summary:

http://www.forbes.com/sites/anthonynitti/2012/12/18/the-corporate-tax-system-is-broken-how-will-president-obama-fix-it/

Please comment on using the velocity of money as an indicator of inflation.

According to the Quantity Theory of Money, price inflation is a function of three variables: the supply of money, the velocity of money and the quantity of economic output. So, yes, velocity plays a part in inflation – but only a part. As a standalone indicator of inflation it’s not particularly useful. (For more, see page 71 of my February powerpoint slide presentation.)

Regarding slides 24 and 29, how much is GDP overstated due to hedonic pricing by the FRB? An overinflated GDP can lead to an understated % of taxes calculation. Perhaps taxes are a larger piece of the pie if hedonic pricing were removed and the statistics were calculated the way they were in the early 1980's. For the real feel to the population, perhaps it would make more sense to calculate taxes as a percent of personal income. (Asked from the viewpoint of a financial planner and not an economist.)

The CBO calculates average federal taxes as a percentage of “market income”, which figure for all taxpayers in 2009 (the most recent year available) was 17.4%, down from 22.7% in 2000. (See page 20 of my February PowerPoint presentation.)

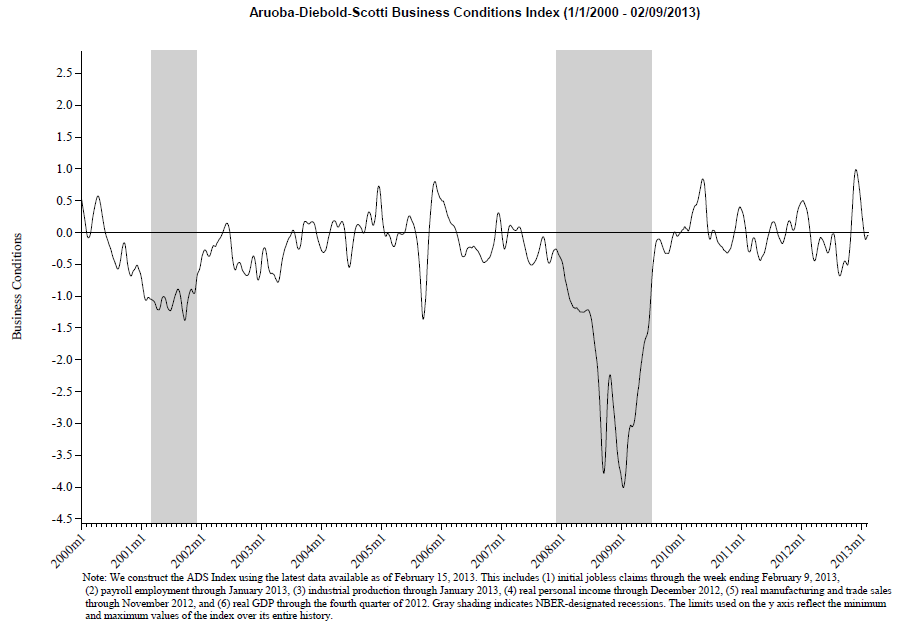

What do you think of the Philly Fed's ADS indicator for forecasting recessions?

Here’s how the Philly Fed describes its ADS indicator: “The Aruoba-Diebold-Scotti business conditions index is designed to track real business conditions at high frequency. Its underlying (seasonally adjusted) economic indicators (weekly initial jobless claims; monthly payroll employment, industrial production, personal income less transfer payments, manufacturing and trade sales; and quarterly real GDP) blend high- and low-frequency information and stock and flow data.”

Below is a picture of the ADS index, with recessions indicated.

Bottom line: it’s a nice summary of current activity but it doesn’t include any elements that are considered forward-looking as do the indexes of leading economic indicators such as the ECRI’s weekly LEI or the Conference Board’s monthly LEI.

Regarding slide about slide 19 or 20, I understand your rational for stronger equity markets, but how do you think the growth in the debt (crisis) will impact the markets, especially with increasing interest rates?

Please refer to the second question, above. Ultimately – and I think trying to assess when a hypothetical tipping point might occur depends on so many variables – markets would react very negatively if it becomes clear that our politicians will never get the strength to make the required changes to the entitlement program spending. But, remember, our system is apt to prove self-correcting as it always has in the past. Which is to say that under a scenario of our politicians not getting the job done, a big selloff in U.S. debt, for example, might be terrifying enough to finally force the required changes.

What do you mean we will have a tax hike? We did have a tax hike?

Yes we did. However, it was a token. ATRA did approximately nothing to solve our deficit problem. (See page 20 of my February powerpoint slide presentation.) That’s why I think the President will be right back to pushing higher taxes.

Please explain the drop in revenues in 2015 on Fed outlays/revenues slide.

Revenues and outlays are expressed as a percentage of GDP in this slide. CBO is projecting slightly faster growth in GDP (the denominator) than in revenues.

How does one dismiss the realization that CAPE P/E is at 23—above the long term average of 15 to 16?

My view is that under present circumstances it makes no sense to use a ten-year average earnings calculation in the denominator of a cyclically adjusted P/E ratio computation. This is because such a ten-year figure would be so grossly distorted by the epic earnings recession of 2008-2009. Keep in mind that, by the CAPE logic, stocks will look cheaper and cheaper as we go forward even if the market goes higher and higher, because those recession-depressed earnings will run off in the denominator.

Far better to use common sense and simply eyeball the market’s historic P/E ratio vs. inflation to determine whether stocks look expensive, or not. (See page 11 of my February powerpoint presentation.)

What are your thoughts on some of the very concerned money managers and their rationale, including Jeremy Grantham, Bob Rodriguez and others, who believe stocks are largely overvalued and are being propped up by the Fed's spigot (with concern over large, perpetual and ongoing debt and deficits)?

See previous question as to the market’s “overvaluation”.

My thought is that it’s an absolutely ridiculous notion.

Re the Fed propping up stock prices, I guess to the extent the Fed is facilitating economic expansion by keeping rates low, they are. This doesn’t mean that when the Fed starts to unwind QE that the economy and stock prices crater. To the contrary. The Fed will start to unwind QE when it has increased confidence in the sustainability of the economic recovery. By definition, that’s a stronger environment for stocks.

Also, my guess is that there’s something to the idea of “the Great Rotation”: when Main Street starts to flee bonds (when yields start to rice) seems like the money might flow towards stocks even as yields are rising.

See comments, above, re the debt and deficits question.

This Website Is For Financial Professionals Only

|

|

|

MEMBER REVIEWS

|

|

|

William Desormeau, Jr.

|

|

It is not possible for me to overstate the cumulative value that Craig, Bob and Fritz have added for over 10 years to my investment advisory practice, as well as for personal and family financial planning. A4A gets my highest recommendation

|

|

|

Lynn Najman, CFP®

|

|

I’ve subscribed to A4A since its inception, and always find it intellectually stimulating and on point. It’s one of the few CE solutions out there that doesn’t waste my time by pushing product or talking down to me.

|

|

|

| Pete Deacon, CPA, CFP® |

| A4A has had a profound effect on my business. Since 2009, I’ve relied on the consistent messaging and updates to run my business successfully. Being able to present the information from Bob, Fritz, and Craig's ongoing CE webinars has been a significant benefit. |

|

|

| Fredric Mayerson, MBA, PhD, CFP® |

| I've been a financial professional and professor of finance for 35 years and find Fritz Meyer and Robert Keebler to be among the most engaging, incredibly knowledgeable, and experienced presenters I’ve encountered. They deliver an extraordinary amount of information in an extremely interesting way — sequentially and developmentally, utilizing pedagogical tools and techniques that few possess. A4A to is the most consistently excellent CE program available. |

|

| Ron Roge, MS, CFP® |

| I’ve been attending A4A many years because the CE classes are outstanding, and my time is valuable. Though I have over 35 years of experience, I’m always learning something new on A4A. I attend fewer conferences now because the CE is generally not advanced. If you want to learn from the best, in a faster, easier, and less expensive way, I highly recommend A4A. |

|

|

John R. Day, CPA/PFS® |

|

I’ve been a member since 2011 and never miss the monthly webinars with Fritz Meyer. I appreciate Fritz’s independent views on the economy and markets and Bob Keebler keeps me updated on excellent tax planning ideas. A4A is a great value! |

|

|

Norman Politziner, CFP |

|

I wouldn't miss a Fritz Meyer webinar unless my pants were on fire. I've relied on Andrew Gluck's knowledge systems --client communications and CE -- for two decades. It's simply the best solution for tax, financial, investment, and risk-management professionals.® |

|

|

|

Dan Hawley, CFP® |

|

A4A, for over a decade, has been a great resource for useful and accurate information and CE. A4A and Advisor Products are bargains for an advisory practice. |

|

|

Kevin Brosious, MBA, CFP®, CPA/PFS® |

|

I get CPA CE credit and CFP credit for the webinars. But not only that, the A4A content is terrific |

|

|

|

|

|

|