The rapid growth in TDFs is a direct result of the Pension Protection Act (PPA) of 2006, which established three Qualified Default Investment Alternatives (QDIAs) for participants who do not make investment elections. TDFs are the most popular choice of QDIA, despite their deficiencies.

Even though TDFs existed prior to the PPA, the proliferation of product is only five years new, so there’s still a lot of room for improvement. One important lesson was learned in 2008 when the typical 2010 fund lost 25%, leading to joint hearings with the Securities and Exchange Commission and Department of Labor in June 2009.

The words “to” and “through” were coined at these hearings. The testifying fund companies explained that they take substantial risk at the target date because their glide paths serve “through” the target date to death. This is in contrast to funds called “to” funds that end at the target date. The clear implication is that “to” funds are far less risky at the target date than “through” funds, but this is not true because the industry has elected to define “to” in a bizarre way, much like President Clinton defined “is.” “To” is being defined as a flat equity allocation beyond the target date. This is unfortunate because the very essence of “to” is the non-existence of “beyond.”

The words “to and “through” were used at the target date fund hearings to mean:

- Through: Target date is a speed bump in the highway of life.

- To: Target date is the end of the investment mission. Accumulation only.

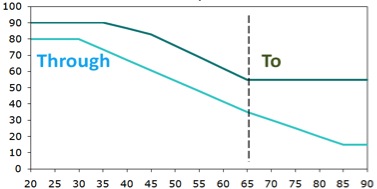

Accordingly, the common belief is that “to” funds hold less equity at the target date because they end there, as shown in the graph on the right.

But “to” funds are being defined as any fund with a flat equity allocation beyond the target date. Why does allocation beyond the target date matter if the intention is to end at that date? The trick is appearing to end without really ending.

The pretext is that any fund that reaches its lowest equity allocation at target date is a “to” fund because changes in the glide path have ended, even though the fund continues on. Fund companies want to keep assets as long as possible, despite emerging investor interest in “to” funds. Fiduciaries believe a “to” fund is safer and more prudent, and it should be. “To” should be safer than “through,” but it might not be, as shown in the graph below.

As a practical matter, the to-through distinction is moot when one considers participant behavior. Most defaulted participants withdraw their accounts at retirement, so most TDFs are de facto “to” funds. The problem is that most are too risky at the target date, even so-called “to” funds. Unfortunately, little has changed since the 2008 debacle, so participants remain exposed to substantial loss as they near retirement. For more on TDFs, visit Target Date Solutions.

Caveat emptor. There will be a repeat of 2008, and this time class action loss-suits are inevitable. Justice will prevail. Attorneys will ask fiduciaries to describe the remedial actions they have taken in their TDF investments to protect participants from a repeat of 2008. Ignoring the past and hoping it’s different the next time is not an option, and it’s certainly not an enlightened view of risk management.

How will you respond?

This Website Is For Financial Professionals Only

|

|

|

MEMBER REVIEWS

|

|

|

William Desormeau, Jr.

|

|

It is not possible for me to overstate the cumulative value that Craig, Bob and Fritz have added for over 10 years to my investment advisory practice, as well as for personal and family financial planning. A4A gets my highest recommendation

|

|

|

Lynn Najman, CFP®

|

|

I’ve subscribed to A4A since its inception, and always find it intellectually stimulating and on point. It’s one of the few CE solutions out there that doesn’t waste my time by pushing product or talking down to me.

|

|

|

| Pete Deacon, CPA, CFP® |

| A4A has had a profound effect on my business. Since 2009, I’ve relied on the consistent messaging and updates to run my business successfully. Being able to present the information from Bob, Fritz, and Craig's ongoing CE webinars has been a significant benefit. |

|

|

| Fredric Mayerson, MBA, PhD, CFP® |

| I've been a financial professional and professor of finance for 35 years and find Fritz Meyer and Robert Keebler to be among the most engaging, incredibly knowledgeable, and experienced presenters I’ve encountered. They deliver an extraordinary amount of information in an extremely interesting way — sequentially and developmentally, utilizing pedagogical tools and techniques that few possess. A4A to is the most consistently excellent CE program available. |

|

| Ron Roge, MS, CFP® |

| I’ve been attending A4A many years because the CE classes are outstanding, and my time is valuable. Though I have over 35 years of experience, I’m always learning something new on A4A. I attend fewer conferences now because the CE is generally not advanced. If you want to learn from the best, in a faster, easier, and less expensive way, I highly recommend A4A. |

|

|

John R. Day, CPA/PFS® |

|

I’ve been a member since 2011 and never miss the monthly webinars with Fritz Meyer. I appreciate Fritz’s independent views on the economy and markets and Bob Keebler keeps me updated on excellent tax planning ideas. A4A is a great value! |

|

|

Norman Politziner, CFP |

|

I wouldn't miss a Fritz Meyer webinar unless my pants were on fire. I've relied on Andrew Gluck's knowledge systems --client communications and CE -- for two decades. It's simply the best solution for tax, financial, investment, and risk-management professionals.® |

|

|

|

Dan Hawley, CFP® |

|

A4A, for over a decade, has been a great resource for useful and accurate information and CE. A4A and Advisor Products are bargains for an advisory practice. |

|

|

Kevin Brosious, MBA, CFP®, CPA/PFS® |

|

I get CPA CE credit and CFP credit for the webinars. But not only that, the A4A content is terrific |

|

|

|

|

|

|