How Savings Affects Retirement Portfoilio In Accumulation And Withdrawal Phases

A client's savings rate is so important but ignored by most advisors in designing portfolios. In this amazing series of studies of portfolio design by Craig Israslsen, Ph.D., this session stands out for its focus on showing the client the effects of different savings rates across his lifespan.

Accumulation results below… Zeroing in on how your clients' savings rate will influence their portfolio's risk. It makes clients choose to behave prudently and appreciate the discipline you enforce. Craig shows how the savings rates affects retirement readiness. Drawing on over 90 years of history and 56 rolling 35-year periods since 1926, he reviews survival rates of retirement portfolios with a range of accumulation and withdrawal rates. He shows the survival rates of portfolios with different risk profiles based on data since 1926, and he tells you how to evaulate the histroic data in making asset allocation decisions. You can make Dr. Israelsen's slides part of your talking points with people ypoiu meet, to explain what you do. You can use his ongoing monthly fact set to fit your own style in emails. newsletters, blogs, and client meetings as well as webinars and seminars.

How could cash have a negative nominal return?

Israelsen: In 1938 90-day T-bills had a nominal return of -0.02%. A negative nominal return rarely occurs. However, there was a money market fund in 2008 that lost money (RPF). It eventually liquidated and investors experienced slight losses. What do you attribute the anomaly in return between the 60% and the 50% portfolios and the 65% 80% stock portfolios?

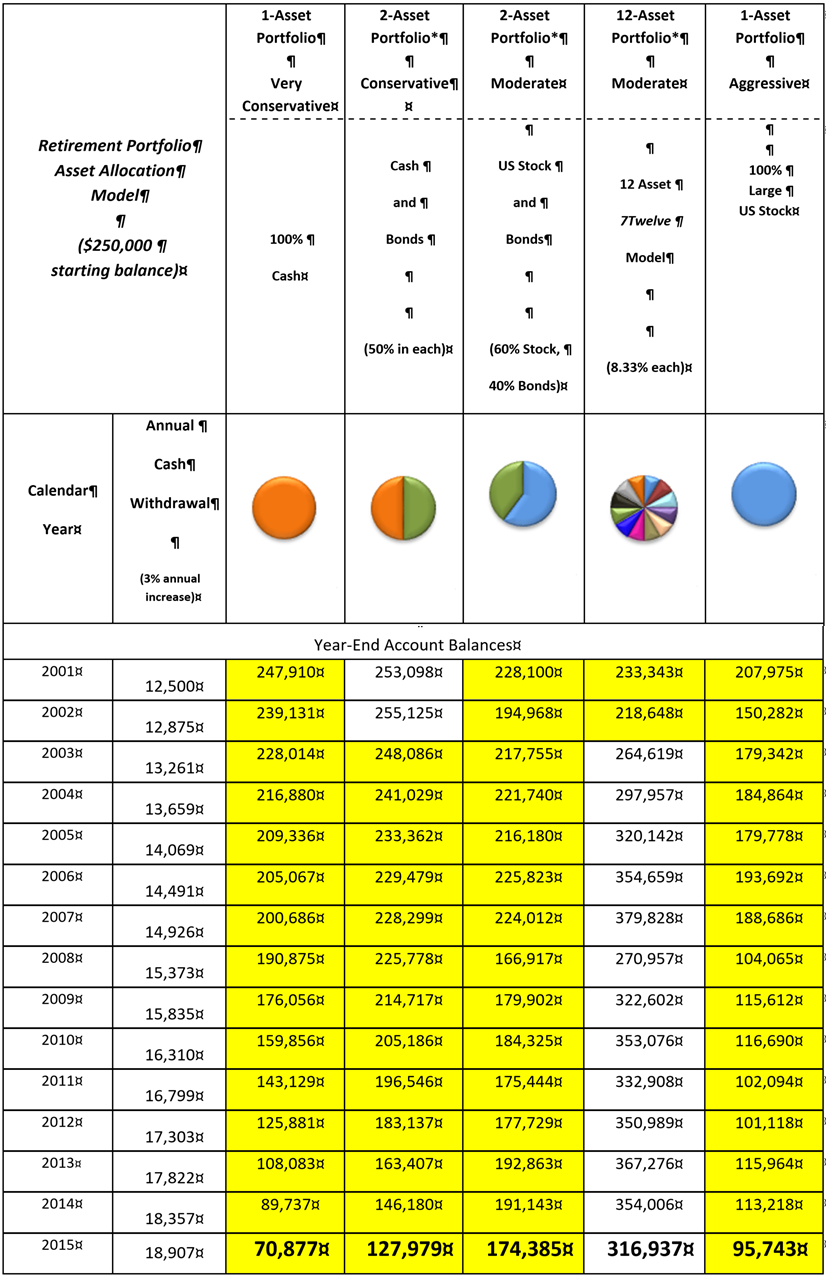

Israelsen: Asset allocation models with only two asset classes (such as the 60% stock/40% bond model or 80% stock/20% bond model) are more susceptible to poor performance of stock because the only other asset class to “help out” is bonds. If both large cap US stock and bonds do poorly at the same time, the two-asset models really suffer. Whereas the 4-asset models—being more diversified—are not as susceptible to the performance of large cap US stock.Do you have an example with your 7Twelve model?

Israelsen: Yes, my March 2016 webinar on A4A covers the 7Twelve model results during the accumulation and distribution phase over the past 15 years. (The 7Twelve model can be performance-tested back to 1998 because TIPS (one of the 12 ingredients of the model) were not “invented” until mid-year 1997.

Do target date funds incorporate the type of diversification you suggest 65/35?

Israelsen: Generally, not in target date funds that are 40+ years from the target date. When target date funds are 10-15 years away from the stated target date they often have an allocation that is approximately 65/35. Thus, some 2030 funds may have roughly a 65/35 allocation today in 2016. These would be target date funds that are more conservative.

Can you incorporate a company match to accompany the savings rate and see how this changes?

Israelsen: Good question. You can use the same table of data and simply add the two together to come up with the total, gross savings rate.

In the current historically low interest rate environment don't you think that the future contribution of the bond allocation going forward at least until rates normalize will be much lower than the historical averages. In other words, stock allocations are more important than ever for success until interest rates rise to more normal levels?

Israelsen: I agree—somewhat. US bond fund returns will likely be lower over the next 10 years than they have been over the past 10 years. But bonds are still an important low-correlation-to-stocks ingredient in a portfolio. Thus, it makes even more sense to diversify into non-US bonds (which are included in the 7Twelve model).

Comments:

Thought provoking.

Very good!

Excellent information

Another excellent and thought provoking webinar by Craig.

I really enjoyed the use of tables, the presentation of how we are approaching portfolios incorrectly, by stating what is your risk, instead of what are you willing to save. Great Stuff

outstanding, he is your best presenter

Today's presentation was a good refresher. I particularly feel that advisors might benefit from Craig's review of the 12X Final Income exercise in several of the earlier slides which illustrates the basic principle of saving an amount equal to 12 times your final salary in order to be able to take 50% of that salary in retirement at a 4% rate. The illustrations and walking everyone through the calculations is helpful. Also good summaries at the end. The methodical and reasoned approach Craig uses is good.

Practical, Clear, Great data to explain benefits of reasonable savings rates, reasonable allocation plans and reasonable withdrawal rates.

Insightful observations every time!

good

great as always with Craig

Excellent

Good review of risk reward and savings rates required.

valuable

it was good

Great charts! I loved how slowly he went over the charts. Too many presenters don't take the time to explain the many numbers on their charts.

Information was good and helpful.

Great

This webinar was very much like another webinar Craig gave earlier this year.

This material should be the lingua franca of every 401k investor education program

This Website Is For Financial Professionals Only