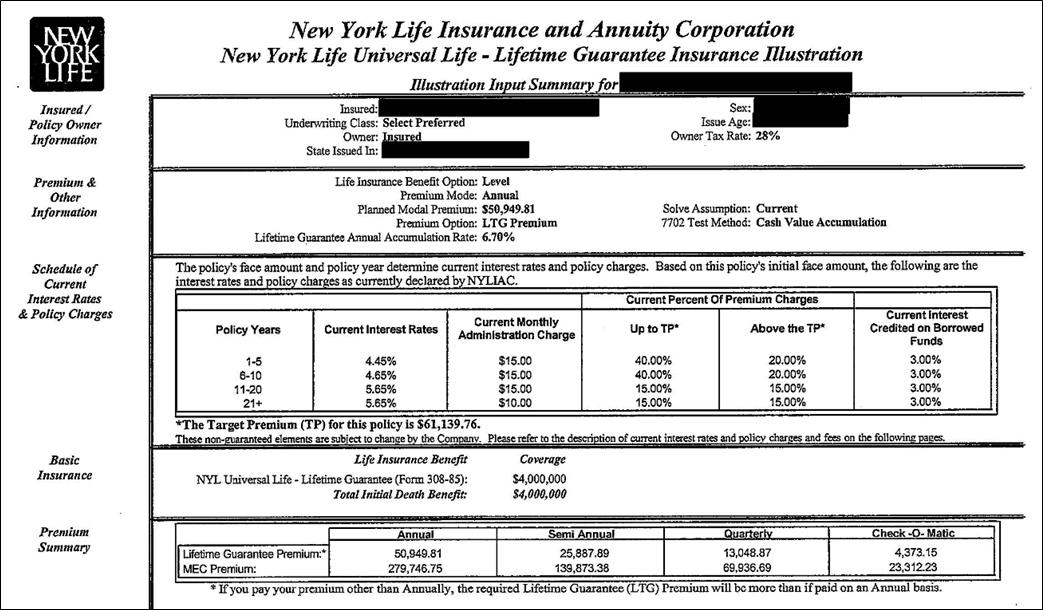

Universal Life – Lifetime Guarantee uses a stipulated premium design for the no-lapse guarantee. The policy remains in force as long as the actual premiums paid accumulated at the Lifetime Guarantee Annual Accumulation Rate exceed the Required Lifetime No Lapse Guaranteed Benefit (NLGB) Monthly Premiums accumulated at the same rate. This comparison of compounded amounts is done each month.

The sales illustration discloses the Lifetime Guarantee Annual Accumulation Rate; in this example, it is 6.70%, guaranteed for the life of the policy. The required monthly premium is $4,373.15, shown in the Premium Summary section as the Check-O-Matic mode of the Lifetime Guarantee Premium. The annual Lifetime Guarantee Premium is $50,949.81, and you can verify that this is the present value of 12 premiums of $4,373.15 discounted at the monthly equivalent of 6.70%.

You have to pay at least $4,373.15 each month, but you can pay more if you choose. To decide if it makes sense to prepay future monthly premiums, you need to know what the discount rate is. In this case, it’s 6.70%, after tax. You also need to estimate the probability of death during the prepayment period, because you don’t get a refund of excess payments at death.

Universal Life – Lifetime Guarantee also has nonguaranteed cash surrender values, which tend to be higher than those for other no-lapse universal life policies. The same page of the sales illustration says that during the first 10 years the current percent-of-premium charge is 40% up to a Target Premium of $61,139.76 and 20% above that, and the charge drops to 15% after 10 years.

There is no surrender charge, so the percent-of-premium charge has a big impact on the cash surrender values. New York Life created an incentive to bunch up the premiums; for example, instead of paying $51,000 each year, you could pay $102,000 in the first year and nothing in the second year. That would reduce the two-year sum of percent-of-premium charges by $8,172, because $40,860.24 of the $102,000 first-year premium would be subject to only a 20% charge. And that cost saving will increase the cash surrender value.

New York Life also created an incentive to skip premiums in Year 10 and pay more in Year 11, because the premium charge will be 15% rather than 40%.

Most consumers probably do not appreciate how much information is shown on this one page. I don’t know how many advisors appreciate it.

This Website Is For Financial Professionals Only

|

|

|

MEMBER REVIEWS

|

|

|

William Desormeau, Jr.

|

|

It is not possible for me to overstate the cumulative value that Craig, Bob and Fritz have added for over 10 years to my investment advisory practice, as well as for personal and family financial planning. A4A gets my highest recommendation

|

|

|

Lynn Najman, CFP®

|

|

I’ve subscribed to A4A since its inception, and always find it intellectually stimulating and on point. It’s one of the few CE solutions out there that doesn’t waste my time by pushing product or talking down to me.

|

|

|

| Pete Deacon, CPA, CFP® |

| A4A has had a profound effect on my business. Since 2009, I’ve relied on the consistent messaging and updates to run my business successfully. Being able to present the information from Bob, Fritz, and Craig's ongoing CE webinars has been a significant benefit. |

|

|

| Fredric Mayerson, MBA, PhD, CFP® |

| I've been a financial professional and professor of finance for 35 years and find Fritz Meyer and Robert Keebler to be among the most engaging, incredibly knowledgeable, and experienced presenters I’ve encountered. They deliver an extraordinary amount of information in an extremely interesting way — sequentially and developmentally, utilizing pedagogical tools and techniques that few possess. A4A to is the most consistently excellent CE program available. |

|

| Ron Roge, MS, CFP® |

| I’ve been attending A4A many years because the CE classes are outstanding, and my time is valuable. Though I have over 35 years of experience, I’m always learning something new on A4A. I attend fewer conferences now because the CE is generally not advanced. If you want to learn from the best, in a faster, easier, and less expensive way, I highly recommend A4A. |

|

|

John R. Day, CPA/PFS® |

|

I’ve been a member since 2011 and never miss the monthly webinars with Fritz Meyer. I appreciate Fritz’s independent views on the economy and markets and Bob Keebler keeps me updated on excellent tax planning ideas. A4A is a great value! |

|

|

Norman Politziner, CFP |

|

I wouldn't miss a Fritz Meyer webinar unless my pants were on fire. I've relied on Andrew Gluck's knowledge systems --client communications and CE -- for two decades. It's simply the best solution for tax, financial, investment, and risk-management professionals.® |

|

|

|

Dan Hawley, CFP® |

|

A4A, for over a decade, has been a great resource for useful and accurate information and CE. A4A and Advisor Products are bargains for an advisory practice. |

|

|

Kevin Brosious, MBA, CFP®, CPA/PFS® |

|

I get CPA CE credit and CFP credit for the webinars. But not only that, the A4A content is terrific |

|

|

|

|

|

|