Estate & Asset Protection Amid Covid Pandemic Hot

Benefiiciaries and grantors in families with taxable estates are likely to face higher taxes, because of the weakening U.S. balance sheet.

Below is the transcript of a continuing professional education class eligible for free continuing education credit to A4A members.

The matters discussed require urgent attention of private wealth advisors, family office professionals, and UHNWIs.

Gideon Rothschild: Hello, and thank you for attending today’s webinar. I am Gideon Rothschild, Co-Chair of Moses & Singer's Private Client Group. With me are my partners, Carole Bass, Daniel Rubin, Irving Sitnick, and Ira Zlotnick. And today we’re going to talk about Navigating a Perfect Storm: Estate and Asset Protection Planning in a Pandemic. As you all know, we’re all sheltered, or we’ve been sheltered for some weeks now. Many clients have been asking about what they should do about updating their documents and whether their documents should be updated, as well as what benefits exist today due to some confluence of factors that we’ve been experiencing, between the low interest rates that we’ll be discussing, depressed values, and the relatively high exemptions for gift and estate taxes. And how can we take advantage of that? So, to start us off this afternoon, I’m going to introduce Carole Bass, who will take us to our first slide.

Rothschild: By the way, if you have questions you’d like to ask, there’s a Q&A button that you can submit your questions through. And at the end we will have, hopefully, some time to take those questions. Thank you. Carole, go ahead.

Carole Bass: Thank you, Gideon. First of all, welcome to everyone, and I hope that everyone on the call and their families are safe and well at this time. The current pandemic has encouraged many people to create or review their estate planning, as we have all been forced to face our own mortality. Also, as a result of the pandemic, our world is changing. And many of these changes will have long-term impact on all aspects of our lives, including on estate and asset protection planning.

Changes in the economy will affect our spending and our lifestyle needs, as well as how wealth is created and depleted. Clients and their beneficiaries may also change residency, as many people are expected to flee from larger, urban areas and from more populous sections of the country out to suburban and rural areas. It’s also anticipated that there’ll be changes in state and federal income and transfer tax as a result of the budget shortfalls from the pandemic. Our current federal estate and gift tax exemption of 11.58 million is already set to sunset on January 1st, 2026, and it will revert to half of the current exemption, but change may come sooner if there’s a change in administration in 2020. So, while it’s an opportune time to do some advance planning and to think about asset protection, all of which we are going to cover later on in the webinar, it’s also an important time to establish or update your core estate planning documents.

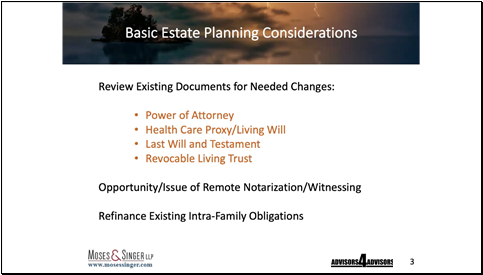

Bass: So, what constitutes this core set of documents? First, a durable power of attorney permits someone else to manage financial matters while you’re living. The power of attorney lets someone else pay bills, write checks, or sell and purchase assets on your behalf. This may be more important now, during the pandemic, for the elderly and infirm who are unable to leave the house, or for those who have become hospitalized.

A health care proxy names someone to make medical decisions if you’re unable to express your wishes. This is really top-of-mind for a lot of people now, understandably. Also, a living will allows you to leave written instructions that explain your health care wishes, especially about end-of-life care. While New York doesn’t have a law governing living wills, our highest court, the Court of Appeals, has stated that living wills are valid as clear and convincing evidence of your wishes. So, it’s important to document these. With those documents, a consideration during the pandemic might be whether there should be someone in the line of agents that you’re appointing who lives in another household, so they wouldn’t be exposed to the virus if you’re exposed. And it’s always important to think through possible future health care scenarios and to have conversations with your family and your friends, or whoever you’re appointing, about your wishes, so that they’re made aware.

A last will and testament and/or revocable trust contains the dispositive provisions that take effect at your death. These should be reviewed to make sure they conform to your current wishes, that your executor and trustee appointments are current, as are the appointment of guardians for minor children. Also, not on the slide but very important, is to be updating beneficiary designations on retirement plans and life insurance policies. Those pass outside of the will or revocable trust, and often people neglect to update those.

With more people than ever trying to complete and execute their estate planning documents, we’ve been forced to find kind of new and innovative ways to get these documents completed while maintaining social distancing. Most frequently, we’ve been arranging for remote video signings for these core documents that I just spoke about. In New York, we have executive orders from Governor Cuomo permitting remote notarization and also permitting certain documents, including those that I just mentioned, to be witnessed remotely. That executive order has now been extended to June 6, and we’ve all become comfortable with that process. It does require some comfort with technology, as clients need to use Zoom, GoToMeeting, or another app that will provide two-way video communication, and then they need to be able to scan the signature pages to the notary and the witnesses on the same day and use Federal Express to get the originals out. If scanning is too complicated, especially for more elderly clients, we’ve been having people snap pictures and text or email those photos. So, there’s always a workaround.

There’s also an ability to do live signings and maintain social distance, especially out in the suburbs, if people can stand far away from each other or do this through windows, either home windows, car windows. There is some concern, however, that once the restrictions on social distancing and the quarantine officially lift, people will still be hesitant to sit in a conference room with three or four other people for what is an old-fashioned signing. We really don’t know if any of these orders on remote witnessing and notarization will stay in effect beyond the shelter-in-place order, so we need to monitor that.

I also want to really quickly mention on this slide, it’s a good time to refinance existing intra-family obligations. The AFR rates are at a historic low, as will be discussed in more detail later. The rates for May are 0.25, 0.58, and 1.15, and they’ll be even lower in June. Next slide.

Bass: More and more often, we’re recommending that clients set up revocable trusts during their lives to avoid probate. And historically, we haven’t done revocable trusts as a matter of course in New York, but that is changing, and started to change before the pandemic, just due to the volume and delays at the court. And on this slide, you’ll see some particular reasons why revocable trusts were used in the past, but it’s become even more important for people to think about avoiding probate. And the pandemic has made this even more clear, as courts for a while were closed and are now only handling limited matters.

So, a revocable trust provides for ease of administration, both at death and in the event of incapacity during life. It avoids the normal time delays you would have in court, and the extent of the delays we have now. But for this to work, the trust has to be funded during life, so you need to retitle assets, including bank and brokerage accounts, real property. Otherwise, you’ll end up probating anyway, to move those assets. As I mentioned, the value of probate avoidance became very clear at the onset of the quarantine. Courts were closed and there was really no means to even get a fiduciary appointed following a death. And the market was falling, and there really needs to be someone in place to secure assets, to be able to sell security, and to marshal funds, especially if there’s a surviving spouse who might need those. So, with that said, I’m going to turn things over to Dan, who’s going to discuss asset protection.

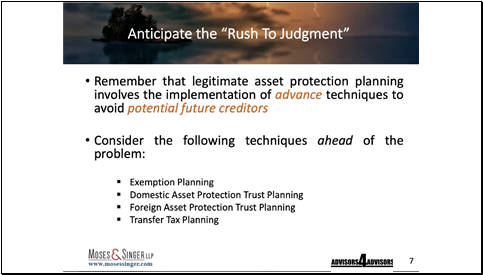

Daniel S. Rubin: Thank you. So, the confluence of factors that exist that make this a good opportunity for estate planning, some of those factors also suggest that this would be an excellent time for clients to consider or reconsider their asset protection planning. Specifically, the economic situation that we find ourselves in, with tenants often not paying their rent, for example, and the personal guarantees that people have signed in favor of the banks and other creditors, which may generate personal liability at some future point in time because of a continuing economic situation, recession or depression, suggests that people should consider whether or not they ought to do what they can at this moment in time, before the problems really come, to protect themselves.

And this definition on this screen, that asset protection planning is the process of implementing advance planning techniques to protect against potential future creditors, has the word “advance” and the phrase “potential future creditors” highlighted and italicized because it’s important. In fact, it’s critical that this planning be done, as all planning must, in advance of a problem, and that it be undertaken only to avoid what are called potential future creditors, not existing or anticipated future creditors. And this suggests that there’s no better time to undertake asset protection planning than this very moment. Let’s take a look at the next slide.

Rubin: The reason why asset protection planning must be done in advance of a problem and to protect only against anticipated future creditors is because of the law of fraudulent transfers, which has sometimes been referred to as fraudulent conveyances or, today, voidable transactions. Essentially, all of those suggest that the law doesn’t permit transfers to be made if they’re done with the intent to hinder, to delay, or to defraud one’s creditors.

And in this regard, the law distinguishes between several different types of creditors. Present creditors and anticipated future creditors, what this slide refers to as subsequent creditors, those two types of creditors are creditors against whom a transfer will either definitely or very likely be found to have been made with the intent to hinder, delay, or defraud. It’s only those potential future creditors, meaning those nameless, faceless persons of whom no awareness exists at the time that the transfer is made, that the law will respect those transfers as not having been made with the intent to hinder, delay, or defraud. So, it’s always important, and especially at this point in time, to engage in this planning as far in advance of a potential creditor problem, so that the creditors that may later complain will be found to be potential future creditors, not existing or anticipated future creditors. Next slide, please.

Rubin: In anticipation of this potential rush to judgment that may come in the next several months or over the course of the next couple of years, what might clients think about doing? Well, this slide suggests that there are probably four things. And we don’t have the time to get into them in any great detail, but let me highlight what these four items, these four bullet points at the bottom of the slide, suggest.

The first is fairly simple exemption planning. That is, converting assets that are completely available to creditors to assets that the law provides are unavailable to creditors because the law, either federal bankruptcy law or state debtor-creditor law, provides should be exempt from creditors. And there are any number of useful sorts of assets into which available assets might be converted. So, for example, a homestead exemption or life insurance or annuities are suggestions of assets that are exempt from creditors, as well as retirement plans. We have techniques whereby assets can be converted into these protected forms of assets without it being deemed to be a fraudulent transfer.

Next would be domestic asset protection trusts, which are currently available in 18 states, by which I mean that there are 18 states that permit domestic asset protection trusts to be established under those states’ law. But I like to say that there are 50 states that permit domestic asset protection trust planning, because the fact that your client is a resident of a state like New York or New Jersey, which don’t provide for domestic asset protection trusts under their own laws, doesn’t mean that if the work is done in advance of a creditor problem, that they can’t establish an effective trust under the law of one of the 18 states that does permit it.

Similarly, residents of any state can create a foreign or offshore asset protection trust to take advantage of the laws of about 20 foreign jurisdictions that permit asset protection trusts. Foreign asset protection trusts might be, or might not be, a better fit for any particular client situation. Certainly, we would think about a foreign asset protection trust for clients who want to place assets, or already have assets, overseas, because they might enjoy a more robust protection from potential future creditors when they have a foreign asset protection trust that’s combined with an asset that’s located overseas.

And finally, we have transfer tax planning, which much of the balance of this webinar is going to address. But the idea is that with the significant exemption of 11.58 million dollars from gift tax, low asset values, and low interest rates, clients should be taking advantage of the opportunity to transfer assets into trusts for estate tax planning purposes. The benefit of transferring assets for estate tax planning purposes is that it avoids, or assists in avoiding, the argument by a disgruntled potential future creditor that the transfer was made with the intent to hinder, to delay, or to defraud them. Instead, of course, it wasn’t done for those purposes. It was done for the purpose of saving the next generation millions of dollars, or tens of millions of dollars, or sometimes hundreds of millions of dollars of estate tax. Next slide and speaker, please, which I think is Irv.

Sitnick: I’m pleased to be speaking. I’ll start again. My limited purpose is to introduce the estate and gift tax planning section of the program. Simply, the goal of estate planning, from a tax perspective, is to transfer assets with as little friction as possible. The friction being taxes—estate, gift, generation-skipping, and income tax planning. The federal government imposes an estate tax on all assets owned by a decedent at a maximum rate of 40 percent. As the slide indicates, our New York area jurisdictions– New York, Connecticut, and New Jersey—have some tax. New York, Connecticut, an estate tax. New Jersey, an inheritance tax.

One of the interesting things about the state tax is that the rules are slightly different than the federal situation. The most important element in the federal estate tax planning now is the existence of an exemption. It’s been mentioned several times before. It’ll be mentioned again. That $11,580,000 exemption is, in effect, funny money. It doesn’t need to go to charity. It doesn’t need to go to the spouse. It can go anywhere one wants, and there is no federal estate tax payable. And it could be transferred during lifetime, and there’s no gift tax applicable to it.

The issues that have been mentioned before, why is this a perfect storm? I think it’s been mentioned several times before, but my own spin on it is that not only are interest rates low, which we will see, and asset values are low, which we will see as well, but we have an election in November. And I think, from my perspective, from a planning perspective, that’s the key point. If there were to be a Democratic House, president, and Senate, it is almost certain that that $11,580,000 exemption would disappear. At the best, it would be reduced by more than half to five million. The rates, at 40 percent, are undoubtedly going to go up. It’s therefore critical for planning purposes that if action is to be taken, it be done this year. Unless one wants to bet on the election. Next slide, please.

Sitnick: This slide is intended to illustrate in a very simple way the advantage of acting now and taking full advantage of the $11.58 million exemption, which, by the way, for husband and wife, is doubled to 23 million dollars. In effect, this slide indicates that if 11,580,000 dollars were transferred in trust, it earned 5 percent a year over 10 years—that’s 5 percent after tax, which could be handled either by exceptional returns or by a grantor trust, which has been mentioned, and which will be mentioned again—at the end of 10 years there’s 18,862,000 dollars of assets remaining. That amount can be transferred to the beneficiaries free of any tax consequences whatsoever.

If, on the other hand, that 11,580,000 dollars had been retained by the transferor, and if he or she died in 10 years, the estate tax payable would’ve been approximately 50 percent at current rate, or 9,400,000 dollars. The transfer to children, assuming that’s where the assets are going, would’ve been reduced from 18 million to 9 million, a 50 percent reduction. This is simply just a very simple illustration of the power of the exemption and why it should be used now. Next slide, please.

Sitnick: The speakers who have preceded me have mentioned several times how low interest rates are. What this chart does is illustrate just how low they are. The Section 7520 rate, which technically is 120 percent of the AFR rate, is simply the rate that the Treasury uses to determine whether a transaction is, in effect, quote, “arm’s length,” end quote, for planning purposes. That rate, as you can see, has been 6 percent, 7 percent. If you go before 1997, it was much hotter. It is currently less than 1 percent. It’s 0.8 percent.

That 7520 rate should be viewed, really, as a hurdle. If an estate planning transaction has assets that generate a return in excess of 0.8 percent—that is, less than one percent—that estate planning arrangement is going to be successful. And it’s fairly obvious it’s a whole lot easier to beat a hurdle rate of less than 1 percent than it would’ve been the 7 percent, for instance, in 1997. The chart simply indicates how much easier it is to have a hurdle rate that can be beaten, and transfer assets, again, with as limited friction as possible. Next chart. Next slide, please.

Rothschild: [laughs] Thank you. So, this is Gideon, by the way. And welcome, everyone. We’re going to now focus on some of the transfer tax planning techniques, and why it’s beneficial to make these gifts sooner rather than later. Of course, someone else mentioned that the exemption is scheduled to be reduced from 11,580,000 to approximately half in 2026, but I frankly believe that whether there is a change in control between the Democrats and the Republicans or not, the exemption will have to go down to finance the expensive programs that the government has been passing to ease the burdens during this pandemic crisis. And they’re going to have to find the money somewhere, and it’s likely going to be most hit among the wealthy population. And so, if the exemption goes down—and in fact, the gift and estate tax rates may very well go up—the advantage of making gifts now, before the exemption goes down, becomes quite evident.

In addition, we have the depressed asset values. The market is down. Business values are down. I had a client the other day who owns a restaurant chain. It’s closed for business. Who would pay a perfect valuation for that business today? So, the ability to make a transfer while there exist significant uncertainties with many closely held businesses, not only publicly held stock or real estate values, for that matter, imposes a bit of urgency at this time. And lastly, removing future appreciation is a big factor. If you can gift away even only three or four million dollars today, and over the next 20 to 30 years, assuming you’re in your 50s, let’s say, a baby boomer in your 60s, still many years to go, all of that appreciation will be removed from the estate tax system.

It also avoids deathbed gift problems. And what I mean by that is, oftentimes the IRS will attack gifts if they are made too soon, too close, to one’s death. And as Dan pointed out earlier, it may protect against future creditor problems that may arise. Not only for the beneficiaries, of course, because if the gifts are made in trust they will obtain absolute creditor protection, but also for the donor. The earlier the gift is made, the more likely it won’t be viewed as a fraudulent transfer. So, we’ve got creditor protection. And then, of course, many of our clients would like to still have the control over the investment decisions and ability to access these assets should they suffer some financial reversal in the future. And so, the next few slides tell us how we might accomplish that as well.

Rothschild: First, let me mention that oftentimes what we recommend, of course, is transferring to a trust rather than outright, especially if one is using up their lifetime exemption. A transfer to a trust will preserve it for future generations, particularly if it’s established in a state that has repealed the rule against perpetuities, which simply means, in lay terms, that if one were to set up a trust in New York, for example, which has not repealed this rule, the trust must end 21 years after those who are alive at the time the trust is established irrevocably die. The last person to die, 21 years thereafter.

Whereas, if you set it up in a state like New Jersey, Pennsylvania, Connecticut, Delaware, Nevada, South Dakota, and many other states that have adopted the more modern approach of repealing the rule and allowing trusts to last in perpetuity, these trusts will be able to benefit future generations forever, as long as the funds last, of course, and without any generation-skipping or transfer tax as each generation dies off, which would not be the case if the assets are transferred outright to a child, let’s say, which then, as that child included those assets in their own estate when they pass away, including any appreciation thereon.

Now, a grantor-type trust is a specific kind of trust that has other benefits to it, including the fact that the grantor, even though the grantor has given up the right to the assets and the income, the grantor still pays the income tax. The advantage to that is if one has a very substantial estate today. Let’s say one has a 50 million estate and wants to deplete it. It’s hard to deplete it. You can use your 11 million exemption, and if married, 23 million and change, but that doesn’t eliminate the balance of the estate that will be subject to estate tax at death. Except that, if it’s a grantor trust, one can deplete their estate gradually, over time, because they will be paying the income taxes on the income, on the earnings that the trust is experiencing. And that is a tax-free gift, in essence, on behalf of the trust, which remains without any tax effect.

If you don’t have a grantor trust today, and the grantor’s still alive, and you want to convert it to a grantor trust, it’s not that difficult. There are ways of doing so, including decanting a trust. It’s simply similar to a decanting of a jug of wine from one entity into another receptacle. Or, if your state doesn’t allow decanting, a nonjudicial settlement agreement may be possible. The other advantage of having a grantor trust is there are certain powers that can be included, such as the power to swap assets with equal value, or the power to receive loans without paying interest or giving security, so that these are ways that the grantor can still have access to these assets while not being a beneficiary of the trust.

And then, you could further leverage the exemption amount. If one were to transfer 11 million of assets as a gift, one could sell additional assets to the same trust, if it’s a grantor trust, without incurring any capital gains tax, because all transfers between a grantor and his or her trust, if they’re grantor trust structures, are ignored for income tax purposes. And what that allows you to do, particularly in this low-interest environment, imagine if I fund a trust with 11 million and I sell another hundred million dollars’ worth of assets to it, or any amount under that, because we like to keep it at almost a ten to one, nine to one ratio.

The assets that are sold to the trust will appreciate inside the trust in a protected environment, and what I receive in exchange is a promissory note, which could have a principal balloon payment out in 20 or 30 years from now, at an interest rate of as low as 1 percent if that transaction is effectuated next month, in June, or 1.15 percent this month, the May rate. Every month the rate changes. It went down for June. And so, I could do this transaction with a 1 percent rate, which means the trust pays me 1 percent interest per year on my $100 million note while the trust is obtaining the benefit of the assets I transferred thereto, which may be appreciating at a 5 or 6 or 7 or 10 percent rate per year. All of that extra appreciation above 1 percent will be kept out of my estate and inure to the benefit of the beneficiaries of the trust. That’s what we call an estate freeze. Next slide, please.

Rothschild: Other ways of obtaining access to these assets that one has given away is by a type of trust commonly referred to as a SLAT, a spousal lifetime access trust, which basically means, for those of you who are married, creating a trust for the benefit of your spouse. And by virtue of that, if a distribution is needed, it could easily be requested from the trustee, and the trustee would distribute it to the spouse, who could then deposit it, obviously, into a joint account, and allow both the grantor and the spouse to enjoy the income or principal from that trust. So, that could be done on a regular basis, if need be. Obviously, that would be depleting the trust, which would be negative estate planning, but the availability is there.

One could also purchase a life insurance policy, noted here as life insurance sidecar, which, if the spouse dies before the grantor, that policy would provide for benefits through a separate trust for the grantor’s benefit, for the grantor’s lifetime, such that it would replace the access that would otherwise have been available in the SLAT. I mention floating spouse. For some people, it might be an appeal if they were to get divorced or widowed and they got remarried. The spouse is defined in the trust instrument as whomever the grantor was married to from time to time. And thereby, the continued access is available if the grantor were to get remarried at a future date.

A ”not quite reciprocal” trust is another way of obtaining access to what you’ve gifted away. And what it simply means is, imagine I set up a trust for my wife. My wife sets up a trust for me. As long as they’re not quite mirror-image trusts, they’re not reciprocal, and we could each use up our respective 11-and-a-half-million-dollar exemptions. And yet, we have these assets still available to us through these not quite reciprocal structures.

Another approach is a special power of appointment trust, or a SPAT. We estate planning attorneys love acronyms—SPATs, SLATs, GRATs, QPRTs, et cetera. You might have heard many of these. But a SPAT is a rather unique device, novel device, which allows for a third party designated in the trust to direct the trustee to make a distribution to someone, let’s say, who’s a descendant of the grantor’s parents. And by doing so, the grantor, even though he’s not a beneficiary of the trust, could receive a distribution simply by that third-party exercise of the power of appointment.

And lastly, we could always consider a self-settled trust, sometimes referred to as a domestic asset protection or foreign asset protection trust, which will allow a person, perhaps who’s not married, to create a trust for their own benefit and use up their exemption that way, but still have access to the trust because they’re a beneficiary. And if the trust is established in one of 19 states or foreign jurisdictions that Dan had referenced to earlier, the trust would not be available to the grantor’s creditors, and thus it could remain out of the grantor’s estate if structured properly. And with that, I believe I will … Well, there are a few other points in the next slide, actually, I’ll make before turning it over to Ira.

Rothschild: And that is that the clients, the grantors, can retain the right to remove and replace the trustees. The trustee can have a decanting power in the trust, so that the trustee can exercise discretion to make some changes based on changing circumstances. One can establish a trust in a jurisdiction that allows quiet trusts, meaning that the beneficiaries don’t even have to get notice of it, perhaps, until they reach a certain age, so that instead of notifying a beneficiary who turns 18 that they have a multimillion-dollar trust they’re a beneficiary of, establishing it in one of these states would avoid that. And lastly, the grantor can, in fact, retain investment control over the assets transferred to the trust, which a lot of clients would prefer to do.

So, there are many different ways to structure these to accommodate a client’s wishes. The key is to do it now, not wait until values recover, or until interest rates start creeping up, or until the exemption is reduced. And with that, I’ll turn it over to my partner, Ira Zlotnick.

Ira Zlotnick: Thank you, Gideon. And hello, everybody. So, one of the key aspects of estate planning involves issues of valuation. In general, when it comes to valuing assets for gift tax purposes, the fair market value of an asset is defined by the IRS in the regulations as the price at which property would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or sell, and both having a reasonable knowledge of relevant facts. When it comes to certain assets, the valuation is obviously fairly straightforward. So, for example, when you have marketable securities, those are very easy to value. They’re based on the value of the high-low of the day. When it comes to other assets, like real estate and business interests, appraisals are typically required to document the values of these types of assets.

When it comes to business interests, the IRS recognizes that discounts are often appropriate. The two most common discounts available to a taxpayer are the discount for lack of control and the discount for lack of marketability. Assume, for example, that you had a 20 percent membership interest in a limited liability company that owned a piece of real estate which had a current value of a million dollars. You might assume that if you gifted away your 20 percent interest, you’d be charged with a gift of 200,000 dollars. However, if you engaged an appraiser to value the gift, he or she could reach a very different conclusion based on the aforementioned discounts. Typically, in fact, an appraiser might say that the value of your 20 percent interest, after the combined discounts for lack of control and lack of marketability, could be anywhere between 60 and 70 percent of the value of the proportionate share of your real estate.

Depending on the nature of the business interest, we might recommend that a client consider recapitalizing the company, prior to making any gift, into voting and non-voting interests, and thereafter transfer his or her non-voting interests to a trust, to benefit from greater discounts. As I previously mentioned, the IRS generally recognizes the applicability of these discounts. And if the gift is audited, the only real question becomes the appropriateness of the size of the discount. At that point, it often becomes a negotiation between the taxpayer and the IRS until some middle ground is reached. But in all events, the discounts are a way of enabling the taxpayer to leverage his or her gift tax exemption. Next slide, please.

Zlotnick: What if you want to gift an asset that’s hard to value, and you’re concerned that the gift might exceed the remaining exemption that you have? Alternatively, what if the appraiser tells you after discounts the gift will not exceed your remaining exemption, but you’re concerned that the IRS might come back on audit and challenge the discounts, and thereby put you into a situation where you have exceeded your exemption? Fortunately, there are a number of different ways to handle this situation.

One of the most common ways to address this concern is by using a GRAT, oftentimes referred to as a grantor retained annuity trust or by the acronym GRAT. This is a statutorily sanctioned trust, whereby the grantor transfers property in trust and retains the right to receive a series of annuity payments for a predetermined period of years. The remaining property left in the GRAT after the annuity term, which is, in effect, all the appreciation in excess of the 7520 rate, which, as we mentioned before, was 0.8 percent for May and scheduled to drop to 0.6 percent in June, will pass to the beneficiaries at virtually no gift tax cost whatsoever.

Most commonly, the GRAT is structured as a zeroed-out GRAT, because the remaindered interest is valued at close to zero for gift tax purposes. Thus, no gift taxes payable, and no gift tax exemption is used in connection with the creation and the funding of the GRAT. To the extent that the investment, again, returns in excess of the 7520 rate, the excess will remain in the GRAT after all the annuity payments have been made, thereby effectuating a tax-free gift.

When a hard-to-value asset is involved, a GRAT can be an extremely useful tool because the GRAT contains a self-adjusting mechanism, which means that if you get the value wrong, the only real consequence is that the annuity coming back to you would need to be adjusted as [inaudible][43:39]. As such, the GRAT makes for a really terrific technique when values are in question.

When dealing with hard-to-value assets, another option would be to make a gift of something less than your remaining exemption amount and leave yourself a cushion, so that any audit and reevaluation by the IRS of the transferred asset would only result in the use of some additional exemption but would not result in any gift tax being owed. If this strategy were employed, you would typically advise the client to file a gift tax return as soon as possible, so as to start the statute of limitations. And you would remind the client to use up his or her remaining exemption, if possible, after the expiration of the statute of limitations.

Another possibility, when it comes to transferring hard-to-value assets, would be to instead have the client gift cash or marketable securities to a trust and then sell hard-to-value assets to the trust for cash or for some combination of cash and a promissory note. One of the primary benefits of structuring the transaction this way is that the gift being reported on the gift tax return is a gift of cash or marketable securities whose value can’t be disputed. We often recommend, however, that the sale component be reported on a gift tax return as well, so as to start the running of the statute of limitations.

Depending on the circumstances, one might want to consider making gifts by way of a formula when gifting an interest in a hard-to-value, closely held business. The idea of the formula clause is to try to ensure that the value of the gift remains below the taxpayer’s remaining exemption amount. Practitioners have used various types of formula clauses over the years, many of which have been challenged by the IRS. But nonetheless, these types of gifts should be considered in certain circumstances. Next slide, please.

Zlotnick: One of the most common ways to structure a trust from an income tax perspective, as Gideon mentioned before, is to structure it as a grantor trust. In simple terms, a grantor trust is a trust in which the grantor usually retains one or more powers over the trust, which causes the trust’s income to be taxable to him or her. These powers can typically be toggled off at some point in the future if, for example, the grantor no longer wishes to be responsible for the trust’s income taxes, at which point the trust would convert into a non-grantor trust and be responsible for its own taxes.

Some of the powers that we draft into our trusts when wanting to ensure grantor trust status is the power for someone to add charitable beneficiaries, a power for the grantor to borrow from the trust without adequate interest or security, and the power for the grantor to substitute property. This last power, the power to substitute property, allows the grantor to exchange property with the trust so long as the exchanged property is of equivalent value. In addition to ensuring grantor trust status, this power provides great flexibility and can be extremely useful if, for example, the grantor, at some point towards the end of his or her life, wants to exchange high-basis property, such as cash, for low-basis property to be able to benefit from the step-up available at death.

As Gideon also mentioned before, from an estate tax perspective, having the grantor treated as the owner of the trust for income tax purposes is also beneficial because it both reduces the grantor’s taxable estate and it also allows for the trust fund to grow income tax-free for the duration of the grantor’s life or, if shorter, the duration of the grantor trust’s term. In addition, since the grantor trust is treated as the grantor’s alter ego for income tax purposes, sale transactions between the grantor and the grantor trust are disregarded for income tax purposes. As a consequence, selling appreciated assets to a grantor trust in exchange for a promissory note has become a very popular estate planning technique over the years, and can serve as an alternative to the GRAT, which Dan is about to discuss.

Rubin: So, this slide is just an excellent example of how powerful a technique a grantor retained annuity trust can be. It suggests that if a 50-year old, which I happen to be 50, took 10 million dollars at a time when the 7520 rate is 1 percent, which is actually higher than it is at the moment—as Irv mentioned, it’s currently 0.8 percent, scheduled to go down next month to 0.6 percent, but let’s say 1 percent—then the two-year, in this example, annuity payment would need to be 5,075,110 dollars. But the property, we would hope, would appreciate at a much more robust rate than a mere 1 percent. Here in our example, we’re assuming an 8 percent rate, and that means that there’s going to be over 1,100,000 dollars remaining in the trust for the benefit of the son here, father’s child, after the two years are up. This is essentially a tax-free, valuation riskless transfer of 11 percent to the next generation. And the value of the father’s gift, as it’s calculated by the IRS, is a mere 13 cents. Let’s go to the next slide, please.

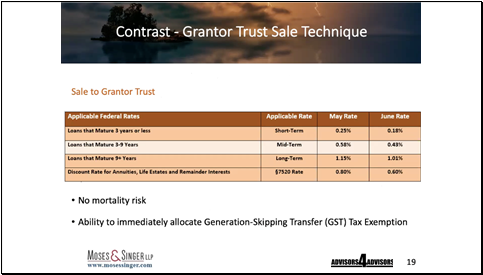

Rubin: This slide demonstrates what’s often an alternative to the GRAT. So, the grantor retained annuity trust and the sale to a grantor trust are often two competing techniques. One of the benefits of a sale to an intentionally defective grantor trust, as it’s sometimes called, is the fact that the sale technique uses the applicable federal rate. And I think, as Irv mentioned earlier, the 7520 rate, which is the rate that’s used in connection with a GRAT, is 120 percent of the federal midterm rate. So, when you have a sale to an intentionally defective grantor trust that’s using the midterm rate as opposed to 120 percent of the midterm rate, you’re going to have a more robust transfer.

This chart at the beginning of the slide shows you what the applicable federal rate is this month, and it shows you what the applicable federal rate is going to be come June 1st. A mere 0.43 percent is the midterm rate, which is the rate that’s used in connection with an obligation that has a term of greater than three years but not greater than nine years. So, you could sell 10 million dollars, hypothetically, of assets to an intentionally defective grantor trust and take back a promissory note that will return to you, the seller, 10 million dollars, with interest at 0.43 percent. We often structure those notes so that they’re interest-only for the first nine years, with a balloon payment of principal at the back end, in order to leverage that very low interest rate.

Rothschild: And, Dan, just to add, a very simple example of how these interest rates can be used is one can establish a grantor trust and simply loan it 10 million dollars, or a million dollars for that matter, on a three-year loan, if you anticipate the market will recover in the next three years. The trust then invests the cash in the stock market and pays back, if you did it in June, 18 basis points to the grantor, the lender to the trust, and it doesn’t require much more than a simple promissory note, and a trust, of course. Of course, you can do the same thing with your children. If you wanted to loan them the 10 million dollars, and you trust them that they’ll pay it back, of course, you only have to get back 18 basis points, and all the appreciation that occurs during that three-year period belongs to them. This is really an opportune time to consider these even simple techniques.

Rubin: Absolutely. Back to the slide, though. Just to contrast a couple of other important differences between the grantor retained annuity trust and the sale to an intentionally defective grantor trust technique, is that the GRAT has a mortality risk, meaning that if you have a two-year annuity term and the grantor were to die within those two years, even if the GRAT would’ve otherwise been successful because, for example, it returned 8 percent and had an annuity paid at the example 1 percent, the mortality risk, the fact that the grantor died in those two years, would mean that the trust was ineffective to put anything outside of his or her estate. With a sale to an intentionally defective grantor trust, the fact of the grantor’s death is not going to automatically return any value. Well, it’s certainly not going to return any additional value to the grantor’s estate.

The other and perhaps the most meaningful benefit, because the mortality risk with a short-term GRAT, for most of our clients, is going to be low, meaning unless you’re in your 90s, that two-year risk is probably not particularly significant, is the idea that you can allocate generation-skipping transfer tax exemption to a trust to which you then sell assets, thereby leveraging the exemption. The Treasury regulations preclude the allocation of generation-skipping transfer tax exemption to a grantor retained annuity trust prior to the conclusion of the annuity period, what’s called the estate tax inclusion period, or ETIP period, which means that GRATS are best used for transfers to the very next generation.

But if we’re talking about substantial clients with substantial wealth and substantial transfers, like an $11.58 million transfer, it may be better to use a grantor trust and a subsequent sale in order that that wealth can be outside of the transfer tax system. Not just for the next generation, but for multiple generations. In fact, perpetually, through the use of a trust that’s set up in a jurisdiction that has repealed the rule against perpetuities. And if we could move on?

Rubin: And the next column, as well. This demonstrates the utility of grantor trust status, whereby the grantor is going to be responsible for paying the income tax on the trust’s taxable income. In both of these columns, you’ll see that the nominal return is 9 percent, but the effective return to the non-grantor trust is a mere 5.8 percent if you account for the fact that the trust, being a non-grantor trust, is going to be responsible for paying its own income tax bill out of its own assets. Where the grantor is responsible for paying the trust’s income tax, you have a nominal rate of 9 percent and an effective rate of 9 percent. And after 20 years of return, that excess return is going to transfer another five million dollars. And after 30 years, it’s going to transfer another 15.7 million dollars of value. So, grantor trusts can be much more effective to transfer more substantial value. And I believe that brings us to the conclusion of our webinar. Next slide.

Rothschild: Well, we have one more slide, actually. But I want to comment on the grantor/non-grantor comparison that may be important to some, and that is that one of the advantages of a non-grantor trust if the grantor lives in a high-tax state is, if structured properly, to avoid state income tax. Of course, if it’s a grantor trust and the grantor lives in New York, he or she is paying New York state income tax on all that income that the trust is earning. If they set up a non-grantor trust and appoint a trustee outside of New York and have no New York source income, the trust would pay the federal tax, but no one would be subject to New York tax, unless of course there’s a distribution to a New York beneficiary. So, at times, there may actually be advantages to looking at this from a different perspective.

Each one of these suggested approaches that we all talked about today really have to be customized to each client’s situation. There is no one size that fits all. And this slide simply demonstrates what we’ve been saying all along, why gifting now is opportune. And even for those who are more moderately wealthy, the ability of structuring these transactions in such a way that one can receive the income or principal of these trusts if need be, through either loans or through having a spouse as a beneficiary, or even using a self-settled trust structure. So, even the moderately wealthy individual should consider availing themselves of these techniques if they have more than 11 million dollars today.

And one simple approach might be if someone had, let’s say, 30 million but wasn’t willing to give away 11 million today. That’s a third of their estate, of their net worth. Consider perhaps transferring 11 million to a trust today, irrevocable trust, but it’s a grantor trust, so maybe next year swap it out for a note, meaning you buy the assets back, provide a promissory note to the trust in exchange. You have an obligation to the trust for whatever the asset value was at the time that you swapped it. And when you pass away, you will have taken advantage of the 11 million exemption, even though you’ve had full use of the assets that were originally transferred. And your estate has a debt that will be deductible on your estate tax return at death. And if the exemption goes down to five million or, as some Democratic proposals want to reduce it, to three and a half million, you will have still availed yourself of the 11-and-a-half-million-dollar current exemption. So, there are things that can be done here.

Q&A Start

Rothschild: We have just about run out of time, but I see two questions here that I think we can answer pretty quickly. One listener asks, “Can I put all my assets in a trust if I’m below the exemption amount?”

Of course, the problem is if you put all your assets into an irrevocable trust for the benefit of a third party, your children, how would you then be able to live? Unless you have independent sources of income, you are receiving a pension, you’re receiving annuities or something of that sort, or your spouse is supporting you. But otherwise, that’s not something you should be doing, because the likelihood is, you’re going to need to retain the income from that. And there’s a section of the Code, 2036, that basically states that if I transfer the tree, I can’t keep the fruit. If it will be includable, the tree will be still includable in my estate.

Another listener asks, “Besides having a third party hold the power to make a distribution to the descendants of the grantor’s grandparents,”—this is referencing what I indicated earlier was a special power of appointment—“are there any other techniques where an unmarried grantor can have her cake and eat it too?”

And as we just described, one way is the strategy I just mentioned. Another way is to have a self-settled asset protection trust, and if need be, the trustee can either make a loan to the grantor at a future time or can actually make a distribution to the grantor because they happen to be a beneficiary. Of course, one needs to be careful that if a distribution is made in a pattern of regular distributions, it will potentially expose the trust to estate inclusion at death. But if that would’ve happened anyway had they not made the transfer to begin with, then there’s no loss, effectively.

So, with that, I thank you all for listening today. I invite you to ask any of our panelists. Send them an email. The email addresses are on your screen. We will have this presentation, if you wanted to listen to it again, on our website in the near future, in the coming days, as well as a copy of the PDF slides that you saw. And I invite you to ask for a consultation with us, if you so desire. And with that, stay safe, wash your hands, and hopefully we will see you soon. Thank you. This concludes our video presentation.