Summer Heat

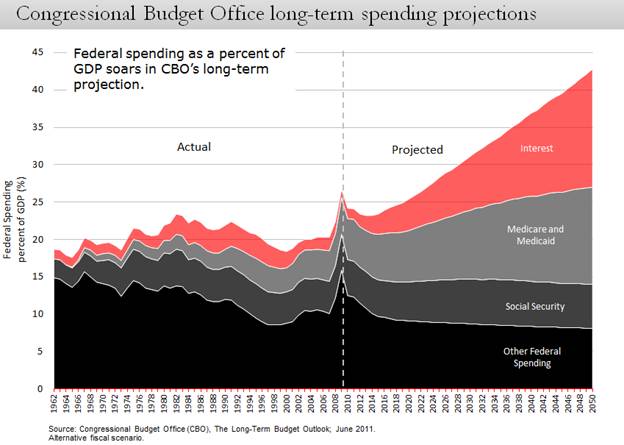

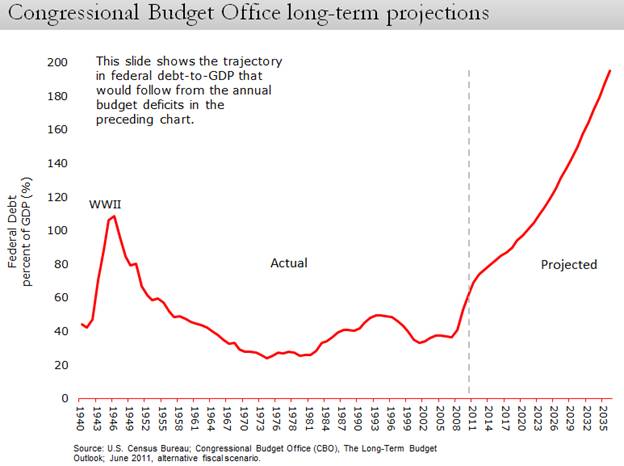

The corollary chart, federal debt ÷ GDP, shows how the U.S. does in fact become Greece without meaningful spending cuts.

Across the Atlantic, yields on Italian and Spanish bonds took an ominous lurch higher, cranking up the heat under the European authorities to provide a credible plan to contain their contagion. On Thursday, the European Central Bank finally acquiesced in its opposition to recognizing a Greek default and debt restructuring, thereby clearing the way for a TARP-like solution to Europe's sovereign debt crisis which, in my opinion, is the only way forward. The European Financial Stability Facility will, as a consequence of allowing the Greek debt restructuring, also have to pony up funds to re-capitalize banks that own the written-down debt, just as the U.S. did. Germany and France will pay more, hence the foot-dragging. But, for now, investors have stopped fleeing the weak European credits and a crucial step forward on the sovereign debt crisis Round II has been taken.

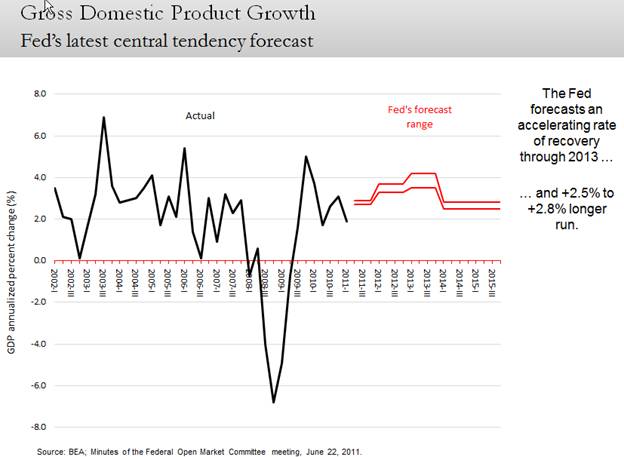

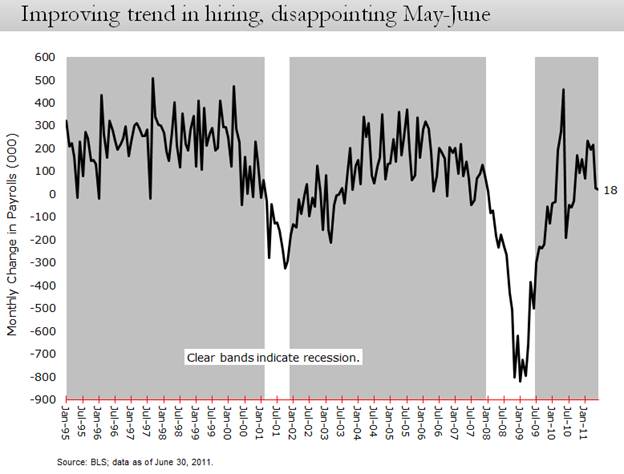

Beside the twin sovereign debt devils, June's stock market swoon was triggered by softer U.S. economic data. Downward revisions to Q2 GDP estimates and the latest jobs report at just +18,000 were the biggest recent blows to investor confidence. Believe it or not, much of the rest of the economic data has been continuing to trend positively. Let's go through the data and I'll show you what I mean.

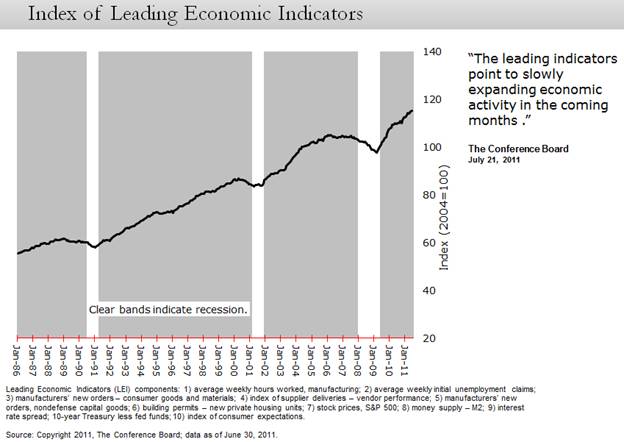

June's index of leading economic indicators, released Friday, ticked higher again. Note how this summer's soft patch is actually a lot less evident than last summer's. Also, see how historically the LEI has decisively rolled over well before a slide into recession. That's clearly not the pattern today.

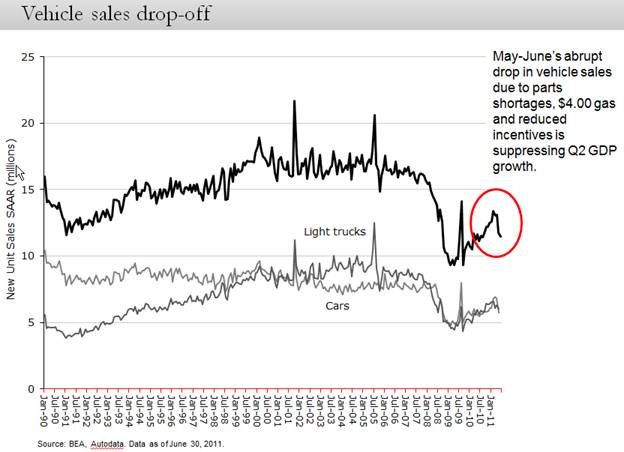

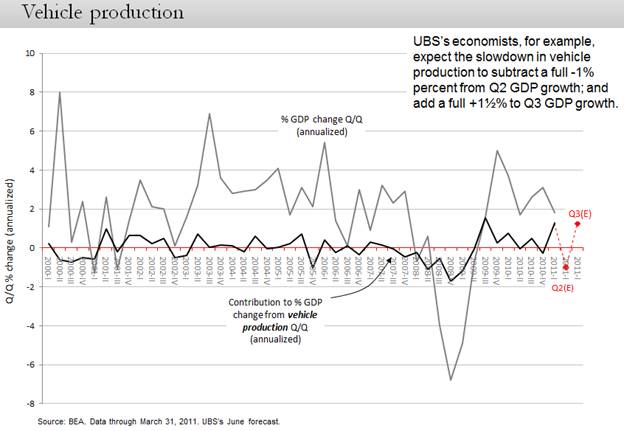

Very significant to this year's summer slowdown was the slump in vehicle production caused by the parts shortage, caused by Japan's earthquake. Car production is already recovering in the second half as parts come back on line. Apart from the near term, the big picture conclusion I reach from this chart is how vehicle production will very likely continue to revert back to "normal" of around 15 million annual run rate. It has to happen, given the average age of the fleet and continued U.S. population growth.

How big of a deal was this auto interruption? A very big deal. In this chart, see how vehicle sales have normally contributed only fractionally to the overall U.S. GDP growth rate of roughly +3%. Now, see how the dramatic drop in Q2 car sales is estimated to have knocked a full percentage point off of Q2 GDP growth. Likewise, it's expected that the Q3 snapback in car sales will give Q3 GDP growth a big boost.

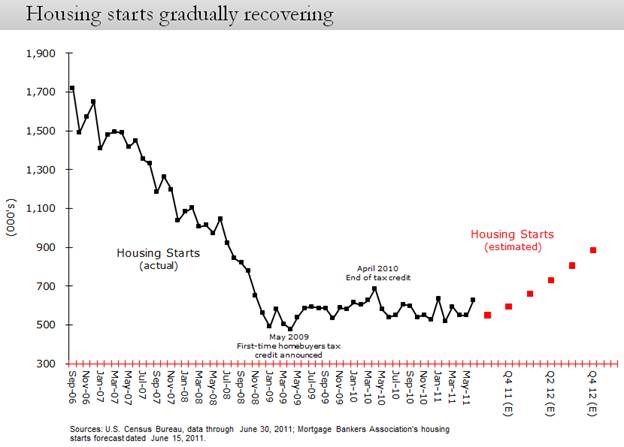

June housing starts were an upside surprise. While housing construction is in the tank compared to the sub-prime mortgage lending boom days, this chart does illustrate the gradual recovery underway.

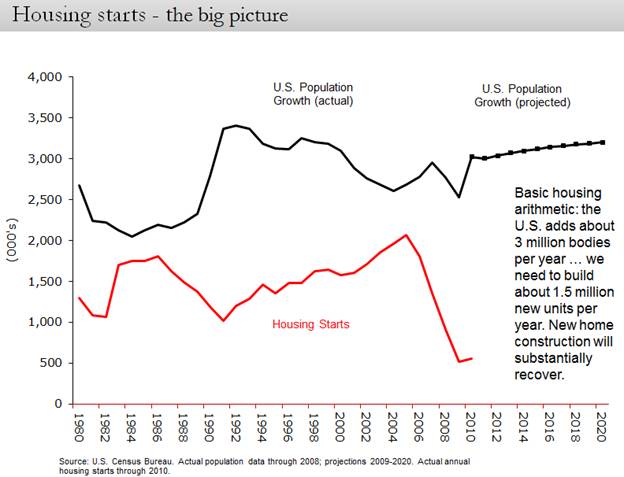

Apart from the recent picture, on the subject of homebuilding remember this basic arithmetic. At bottom, the demand for shelter is a demographic function. Historically and projected, the U.S. adds roughly 3 million to its population each year which has translated into annual demand for new units of roughly 1.5 million. We were overbuilding during the boom. We've been underbuilding, working off the excess inventory now for several years. The bottom line is that starts must gradually, eventually, revert back toward 1.5 million as pent-up demand continues to build. That's almost triple the latest monthly run rate.

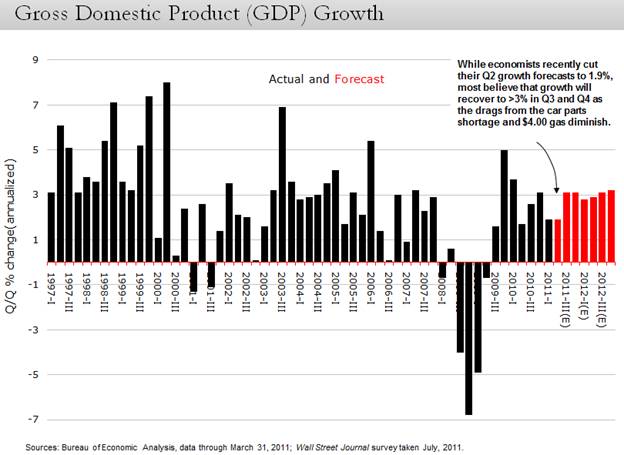

A snap-back in vehicle sales, continued gains in disposable personal income and spending, a small contribution from rising construction – these are some of the key reasons why the 55 best and brightest economists just surveyed by the Wall Street Journal also on average conclude that the first half's soft patch will likely transition into second half re-acceleration. See the red bars in the chart, below.

With last week's release by the FOMC of their June 22 meeting notes the Fed illustrated that they, too, are sticking with their story: expect growth to re-accelerate in the second half of 2011 and 2012.

Back to some important aspects of the very disappointing June jobs figure. First, note how the monthly new jobs number has, in all historic periods, been very, very volatile. Second, note how, for example, coming out of the last recession, net new job formation went from plus 100,000 in 2002 to minus 250,000 in 2003.

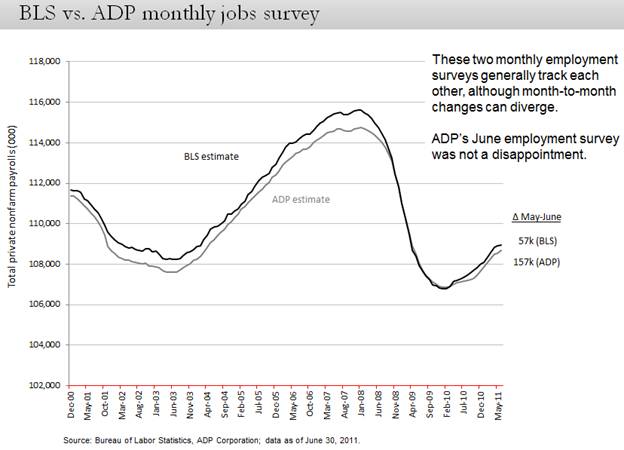

Third point on June jobs. Whereas the BLS's number was weak, ADP's number was not – and the two do track one another through time.

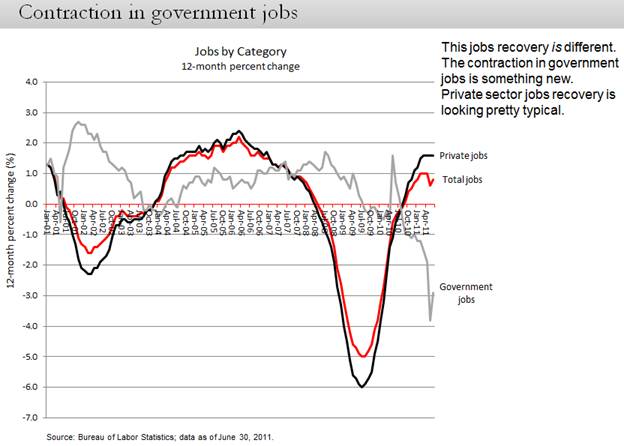

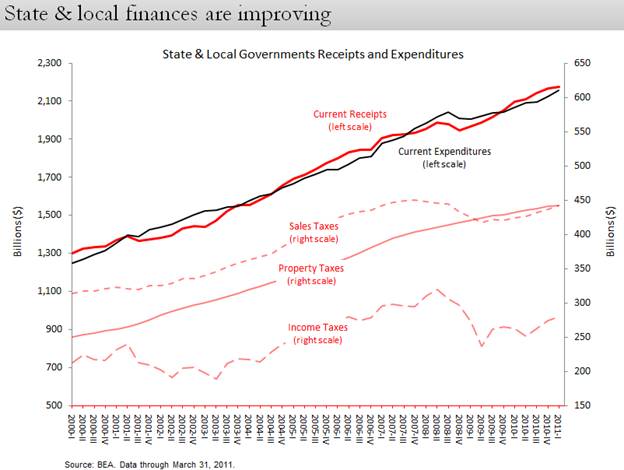

Finally and most significantly on June jobs, this chart reveals how net job formation has been so significantly impacted by the contraction in government jobs, whereas the private sector pattern looks pretty typical for this stage of recovery. A) while painful in the short term, this is a necessary and good downsizing of the public sector, in my opinion; and, B) it's likely that most government job layoffs are already behind us – the U.S. postal service layoffs and all the state and local jobs that had to be cut in order to balance their 2012 budgets beginning the fiscal year at July 1, 2011.

Probably state and local jobs will stabilize going forward as their budgets have come back into balance.

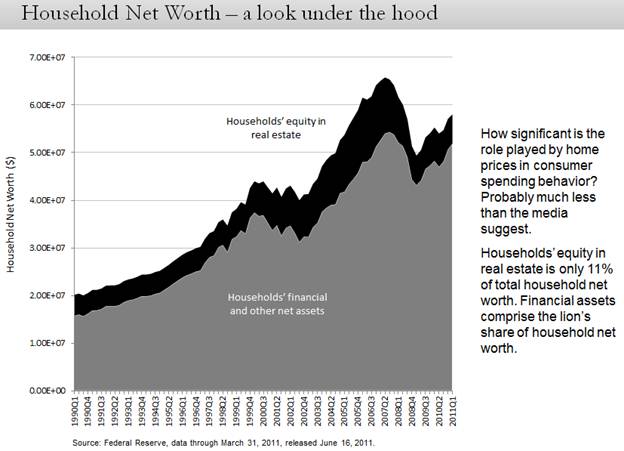

Finally, before I leave the economic data, this observation on house prices. With every month's release of the Case-Shiller and other home price indices I hear a lot of hand-wringing on financial TV about how moribund home values will stifle a recovery in consumer spending. But, here's the fact: contrary to popular myth, home prices are pretty irrelevant to consumer spending. First, take a look at the following chart that illustrates how, in fact, small a piece of household net worth is actually represented by households' equity in real estate.

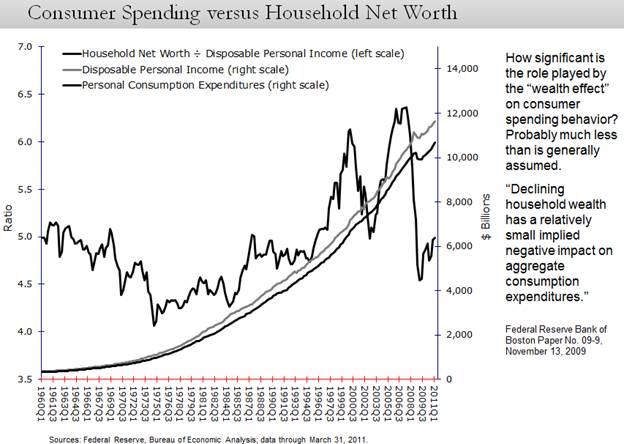

Second, take a look at how it is disposable personal income, period, that drives personal consumption expenditures – and how little the changes in household net worth have to do with spending behavior.

"Sell in May and go away" was looking smart through most of June but, lo and behold, here in mid-July the stock market is right back up within 1½% of its post-recession high. Stocks continue to take the punches mighty stoically – and are behaving rationally – given what I think will be continued improvement in the underlying fundamentals.

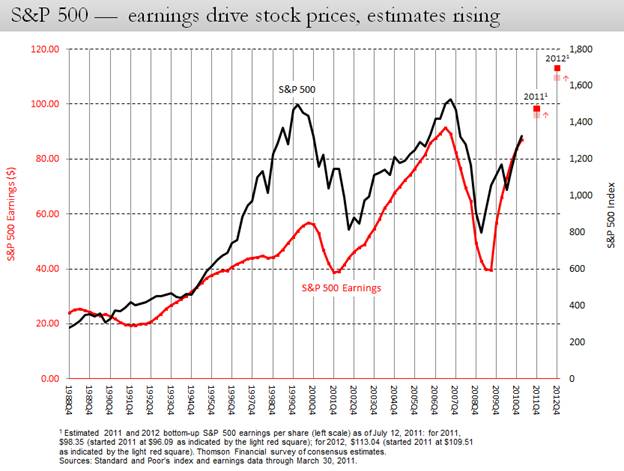

Plotting today's S&P 500 earnings estimates against the Index results in the following chart. If we come anywhere close to the forecasted ~$98 per share in earnings this year, I have to believe the Index will end the year a good deal higher than at 1345 where it closed Friday. Most Wall Street strategists have year-end targets between 1400 and 1500, for which this chart provides a clear rationale. A reasonable market P/E ratio of 15 applied to $98 in earnings would put the index at 1470.

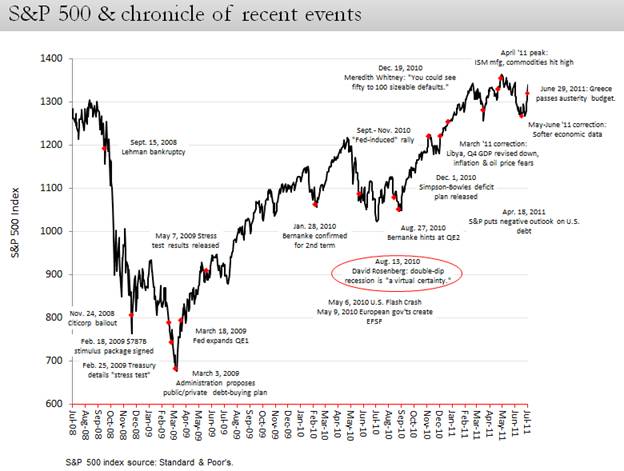

I just want to pass along a chart that I've recently inaugurated that keeps a running chronicle of market-related events. It's a moving picture of the Wall of Worry. I constructed it because it always seems that the latest crisis is so bad. The chart serves as a reminder, for example, of what we were worrying about last year at this time – and that was 29%-ago on the S&P 500. The punch line is that yesterday's hurdles did turn out to be surmountable. In the big scheme of things that is always the case. Not to be too harsh on one particular guy who likes to make bold predictions, but note how Dave Rosenberg precisely bottom-ticked the stock market with his dire double-dip pronouncement a year ago. I pulled it up because I get a lot of "yes, but, Dave Rosenberg says …". If you've listened to my monthly webinars you know the conviction (and evidence) I have in the notion that Wall Street gurus cannot systematically add alpha with their forecasts. Hence, Modern Portfolio Theory – staying fully invested in a diversified portfolio with periodic rebalancing – is still the best investing mousetrap yet devised.

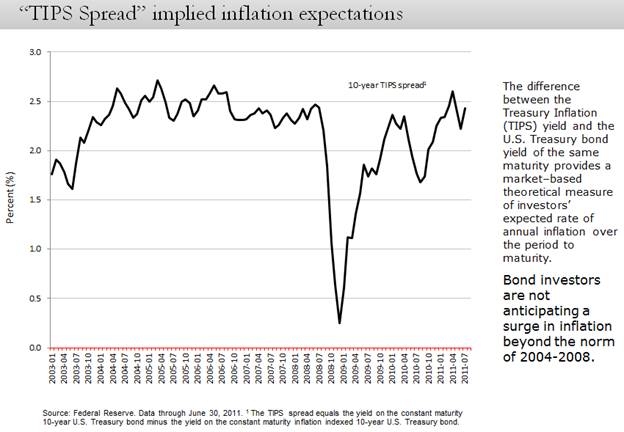

Inflation anxiety has ebbed this summer, with concerns over the soft patch, lower crude oil, Europe's sovereign debt crisis and China's efforts to brake economic growth and break inflation. In this chart, see in the TIPS spread – the best market-based measure of 10-year inflation expectations – the market's complacency over inflation prospects.

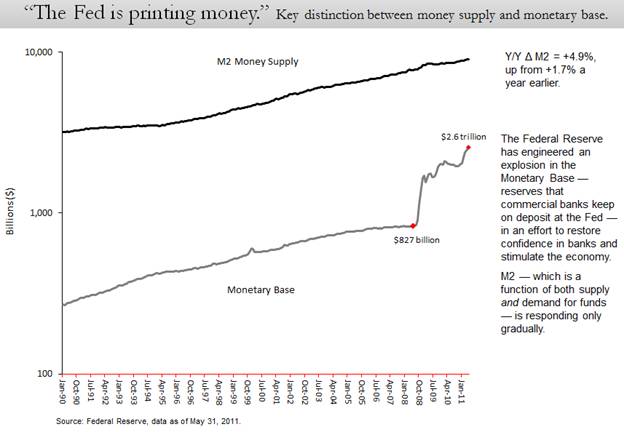

Ah, you might say, but what about the Fed's printing all of that money? Recognize the key distinction in terms: monetary base vs money supply. The Fed has, indeed, exploded the monetary base – but which has thus far only resulted in modestly moving the needle on money supply. Unless and until the rate of growth in money supply substantially accelerates there cannot be a big step-up in final demand chasing, let's call it, a fixed supply of goods and services. Money supply – the stock of cash, checking, savings and retail money market accounts – is the key. It's the measure of aggregate buying power. This is why the Fed continues to say, in effect, "don't sweat a big inflation surge."

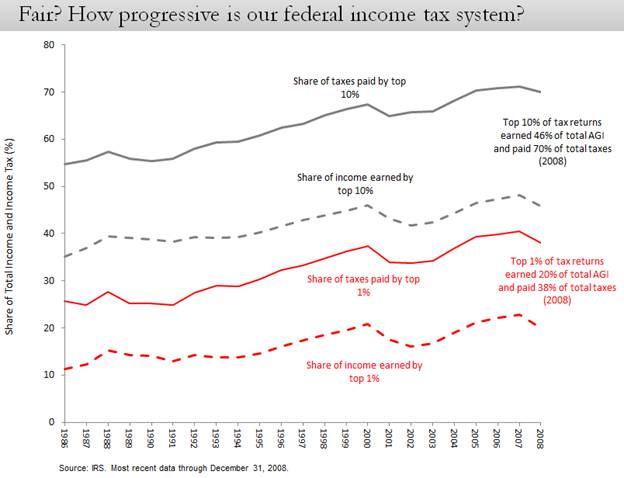

I'll wrap up this month's notes with a comment on taxes, as that subject will be in the headlines as long as the U.S. deficit and debt crisis remains unresolved. The administration's position is that the tax code should be more "fair" … so taxes on the highest earners should go back up to pre-Bush tax cut rates. Today the top 1% of earners account for 20% of total adjusted gross income (AGI) and pay 38% of total income taxes. The top 10% earn 46% of total AGI and pay 70% of total income taxes. The share of both AGI and total taxes paid by the highest earners has risen steadily over recent decades and the proportion of one to the other, if anything, has become slightly more progressive. See the chart. I just want to get this data in front of you because I think the moral argument against more "fairness" is a good one: why should the system be made any more progressive than it currently is, particularly when the bottom 50% of earners pay no income taxes? Also, the data suggest to me that the system is certainly no less fair today than it was in 1986. You decide. "Fairness" is definitely in the eye of the beholder.

As for the economic consequences of higher taxes, as Bernie Marcus, co-founder of Home Depot, said last week, "even brain-dead economists understand that when you raise taxes, you cost jobs."

This Website Is For Financial Professionals Only